Answer:

<u>to keep their prices the same</u>

Explanation:

Remember, having a higher Menu cost implies that such a firm would suffer more if it adjusted its prices.

So the sticky-price theory makes the assumption that a firm that notices an increase in the prices of their products would <em>keep their prices low</em> out of fear that doing so would result in losses for the firm if demand changes negatively.

I believe the correct answer from the choices listed above is option C. It should be Nuttall that be filed directly after nigel. Other given options are filed before Nigel when alphabetical order is followed. Hope this answers the question. Have a nice day.

Answer:

The correct answer is letter "B": Identification of cost pools, identification of cost drivers, calculation of pool rates, assignment of cost to products.

Explanation:

Activity-Based Costing or ABC is a managerial accounting method that assigns certain indirect costs to the products incurring the bulk of those costs. ABC is primarily used in the manufacturing sector to make a better calculation of the true cost of production per unit. For that purpose, ABC follows this sequence:

1) Identification of the activities for the creation of the product

2) Divide the activities into cost pools

3) Assign each cost pool to a cost driver

4) Calculation of the cost driver rates

5) Assignment of cost to products

Answer:

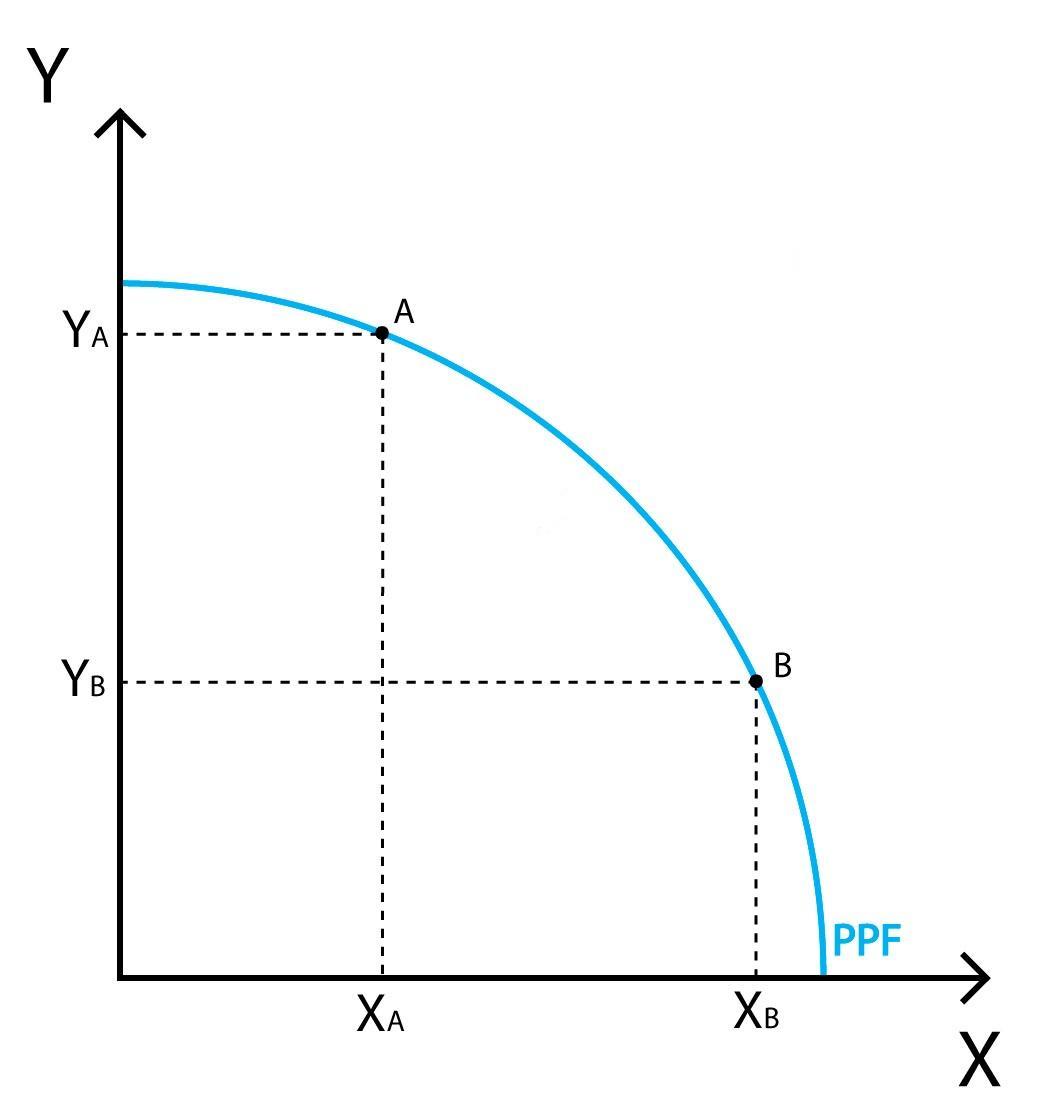

E) bowed out shape of the production possibilities frontier.

Explanation:

The production possibilities frontier curve is usually has a bowed out shape because as the production of one of the products increases, the opportunity cost of producing the other product also increases.

As shown in the attached image, as the production of Y increases, the opportunity cost of producing X will also increase, giving the curve a bowed shape. The same happens to the opportunity cost of producing Y when the production of X increases.

Answer:

1. Lower the interest rates in the economy.

2. Increase asset prices

Explanation:

Remember, increase in money supply looks at the total money made available in circulation in an economy. Alternatively it is called liquidation.

The real of an economy takes into consideration the impact of inflation on the value of goods and services produced in an economy.

Therefore lower interest rates as a result of increase in money supply would results in more consumption and borrowing.

While the price of houses, stocks would rise because of the increased money supply.