Full question attached:

Answer attached

Answer and Explanation:

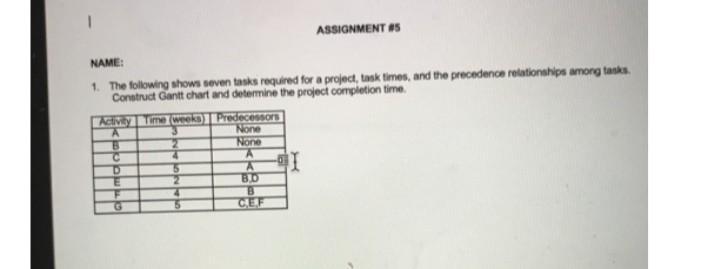

ES= earliest start time

LS=latest start time

EF= earliest finish time

LF= latest finish time

in calculating earliest start time, we look at predecessor to the task, for example c has a predecessor of A and so ES would be after A=3.in calculating our earliest start time and latest finish time we have used the forward pass and backward pass method respectively. The forward pass method uses the latest of the predecessors earliest finish in calculating ES while the backward pass method uses the earliest of the successors latest start(LS)in calculating latest finish(LF)

EF=ES+time

LS=LF-time

slack=LF-EF

The Critical path is ADEG identified by zero slacks

project duration is equal to duration of critical path equal to 15

Character of the business partners. The people behind an idea or company and, more importantly, their character is extremely important. ...

Capacity of the business partners. ...

Innovative idea. ...

Communal benefit. ...

Long-term sustainability. ...

Financial outlook.

Answer:Addition to net income in the operating activities section

Explanation:

A=2610 you didn’t show the question but I help for nomber one