Answer: The correct answer is option B: Equilibrium price and quantity will both increase

Explanation: First and foremost, a definition of demand would be in order. Demand can be defined in simple terms as the quantity of goods or services that consumers are willing and able to buy at a given price and at a particular point in time. The law of demand states that, "All things being equal, the higher the price of a commodity, the lower the quantity demanded by the consumers, and the lower the price of the commodity, the higher the quantity demanded by consumers." This is theoretical and is the ideal situation for a rational consumer.

However, producers (sellers) are only willing to supply more if the price is higher (for the sake of profit of course) and are willing to supply less if the price is lower. This shows that there is an inverse relationship between both variables, that is, at a higher price the producer wants to sell more while the consumer wants to buy less, and at a lower price the producer wants to sell less while the consumer wants to buy more. It gets to a point where they both have to compromise and agree on a price suitable to both producer and consumer, and that in economics is the equilibrium price.

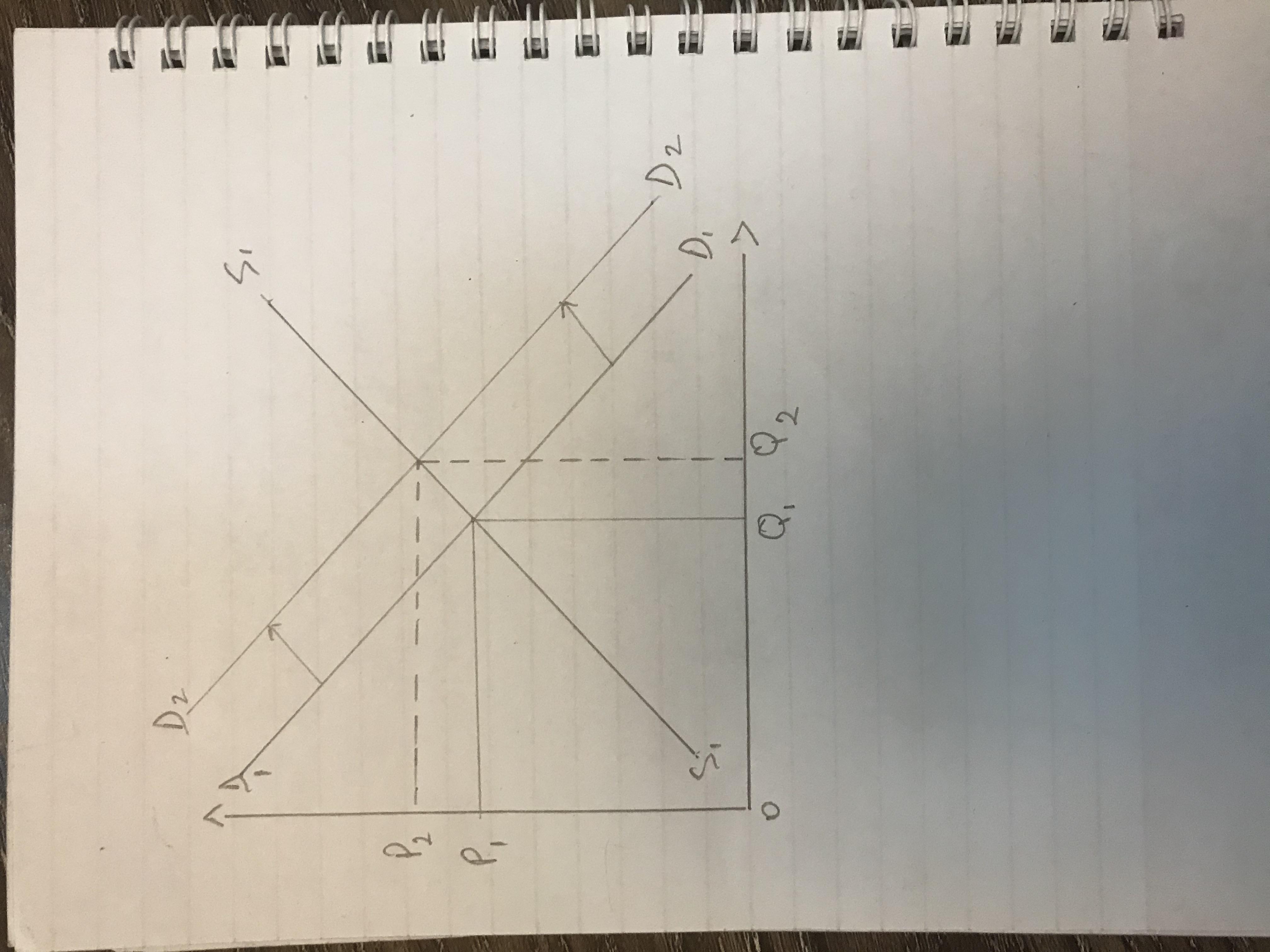

As shown in the attached diagram, the equilibrium price is P1, while the equilibrium quantity is Q1.

In economics theory, a number of factors are usually responsible for a change in the market demand and one of such is population. Take for instance, in a community with 1000 individuals making up the market demand for commodity A, an increase in the population to 1500 individuals would mean that the number of consumers has increased considerably. Consequently the market demand would also increase. However, there would be an excess of demand over supply, that is, the increased demand cannot be met by the current level of supply. Hence the appropriate response to the pressure shall be an increase in the price on the part of the producers. As shown in the diagram, the demand has now increased from D1D1 to D2D2 and the equilibrium price has also changed from P1 to P2. This is because, the increase in population that led to the increase in demand has now resulted in a new equilibrium point as shown by the intersection of D2D2 and S1S1.

Therefore, the new equilibrium price is now P2 and the new equilibrium quantity is now Q2