Answer:

Explanation:

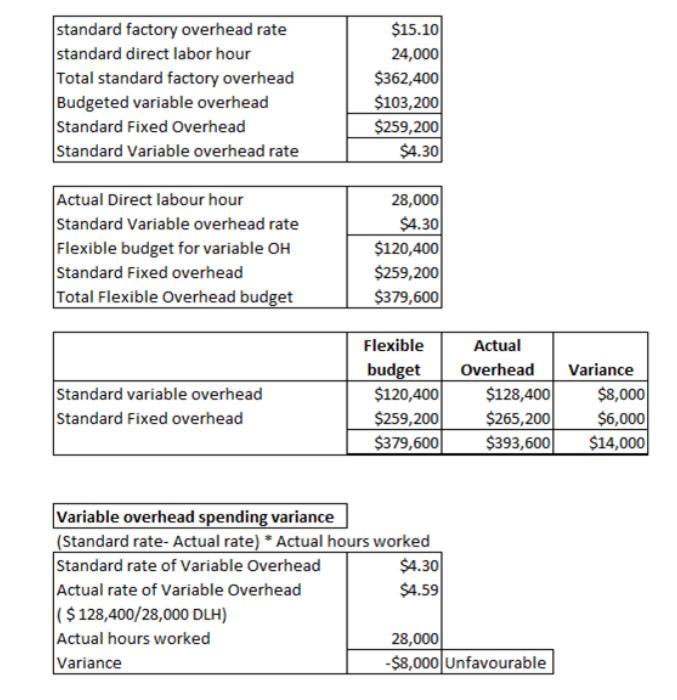

check attached file for solution

Answer:

they can receive more work for less pay from the servants as opposed to the wage workers

Explanation:

Based on the information provided within the question it can be said that they preferred servants' labor more because they can receive more work for less pay from the servants as opposed to the wage workers. At that time roughly four months of workers' wages would pay for about five or six years of servant labor, thus leading to a massive increase in savings for the employer.

Paying your phone bill late and maxing out your credit cards will hurt your credit... So it should be 1 and 3 :)

Answer:

B) $59,500

Explanation:

The equipment was purchased for 85,000 and has no salvage value which means that all 85,000 will be depreciated over it lifetime. It has a life of 5 years and because it uses straight line method it means that it will depreciate equally each year. The equipment is bought on JAN 1 2010 and sold on July 1 2013 which means that the equipment is used for 3.5 years and in order to find its depreciation we will divide 3.5 by 5 and multiply it by 85,000.

3.5/5*85,000=59,500

Answer:

Profit making and survival

Explanation:

The main objectives that a business might have are: Survival – a short term objective, probably for small business just starting out, or when a new firm enters the market or at a time of crisis. Profit maximisation – try to make the most profit possible – most like to be the aim of the owners and shareholders.