Answer:

Answer for the question is given in the attachment

Explanation:

Answer:

7.8%

Explanation:

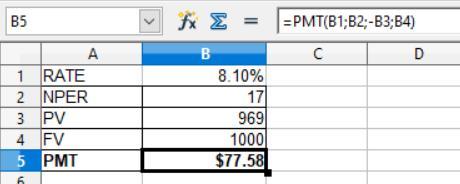

For computing the coupon rate first we have to determine the PMT by using the PMT formula which is shown in the attachment below:

Given that,

Present value = $969

Future value or Face value = $1,000

RATE =8.1%

NPER = 17 years

The formula is shown below:

= PMT(RATE;NPER;-PV;FV;type)

The present value come in negative

So, after applying the above formula, the PMT is $77.58

Now the coupon rate is

= $77.58 ÷ $1,000

= 7.8%

The popularity of social media sometimes leads to a new stage in the hierarchy of effects known as advocacy where loyal consumers recommend brands they have adopted.

the question is incomplete .please read below to find the missing content

The popularity of social media sometimes leads to a new stage in the hierarchy of effects known as ________ where loyal consumers recommend brands they have adopted.

Multiple Choice

evaluation

advocacy

preference

interest

repurchase

Advocacy is the activity of individuals or groups aimed at influencing decisions within political, economic, and social institutions. Advocacy Her group, for example, is a non-profit organization dedicated to helping women who have been victims of domestic violence and are afraid to speak up for themselves.

Advocacy includes promoting the interests or causes of someone or a group of people. An advocate is someone who advocates, endorses, or supports a cause or policy. Advocacy is also about helping people find their voice. There are three types of advocacy: self-advocacy, individual advocacy, and system advocacy.

Learn more about advocacy here

brainly.com/question/1086036

#SPJ4

Answer:

True

Explanation:

The variables price and quantity are inverse correlated then a change in 1 has the exact opposite effect in the other.

False The reporting requirements in SARA Title III require many businesses to file annual reports listing the estimated quantities of both routine and accidental releases of listed toxic chemicals

<h3>What is

SARA Title III ?</h3>

Title III of the Superfund Amendments and Reauthorization Act (SARA), also known as the Emergency Planning and Community Right-to-Know Act (EPCRA), requires states and local governments to establish local chemical emergency preparedness programs for their communities.

Title III of SARA is the Emergency Planning and Community Right-to-Know Act (SARA Title III) (EPCRA). SARA Title III mandates emergency planning and Community Right-to-Know reporting on hazardous and toxic chemicals for federal, state, and local governments, Indian tribes, and industry.

On October 17, 1986, the Superfund Amendments and Reauthorization Act (SARA) amended the Comprehensive Environmental Response, Compensation, and Liability Act of 1980 (CERCLA).

To know more about SARA Title III follow the link:

brainly.com/question/25689052

#SPJ4