Answer:

True.

Explanation:

Yes, this is true that the primary objective of the Uniform Electronic Transaction Act (UETA) is to eliminate the barriers to e-commerce by providing the same legal impacts to electronic records and signatures as is currently provided to paper documents and signatures, but following are the condition which must be fulfilled :

Unique to the signer

Fitted of being verified

Under the signer’s sole authority

Linked to the record in a way that it can be arranged if anything in the document was changed after the signature was stamped

Designed by a reliable means for the object in which the signature was applied.

Answer:

"free market economy" or "free enterprise economy"

Explanation:

Answer:

The correct answer is letter "D": Charging the stolen asset to an expense account.

Explanation:

An asset misappropriation takes place when individuals take advantage of the job position they have in order to profit from fraudulent activities. The fraud could be caused by any employee within a given organization, from high executives to any of their subordinates.

In the case, option "D" is a good example of asset misappropriation since it is being charged to an expense account a good that was stolen when that kind of account is only useful to report work-related expenses.

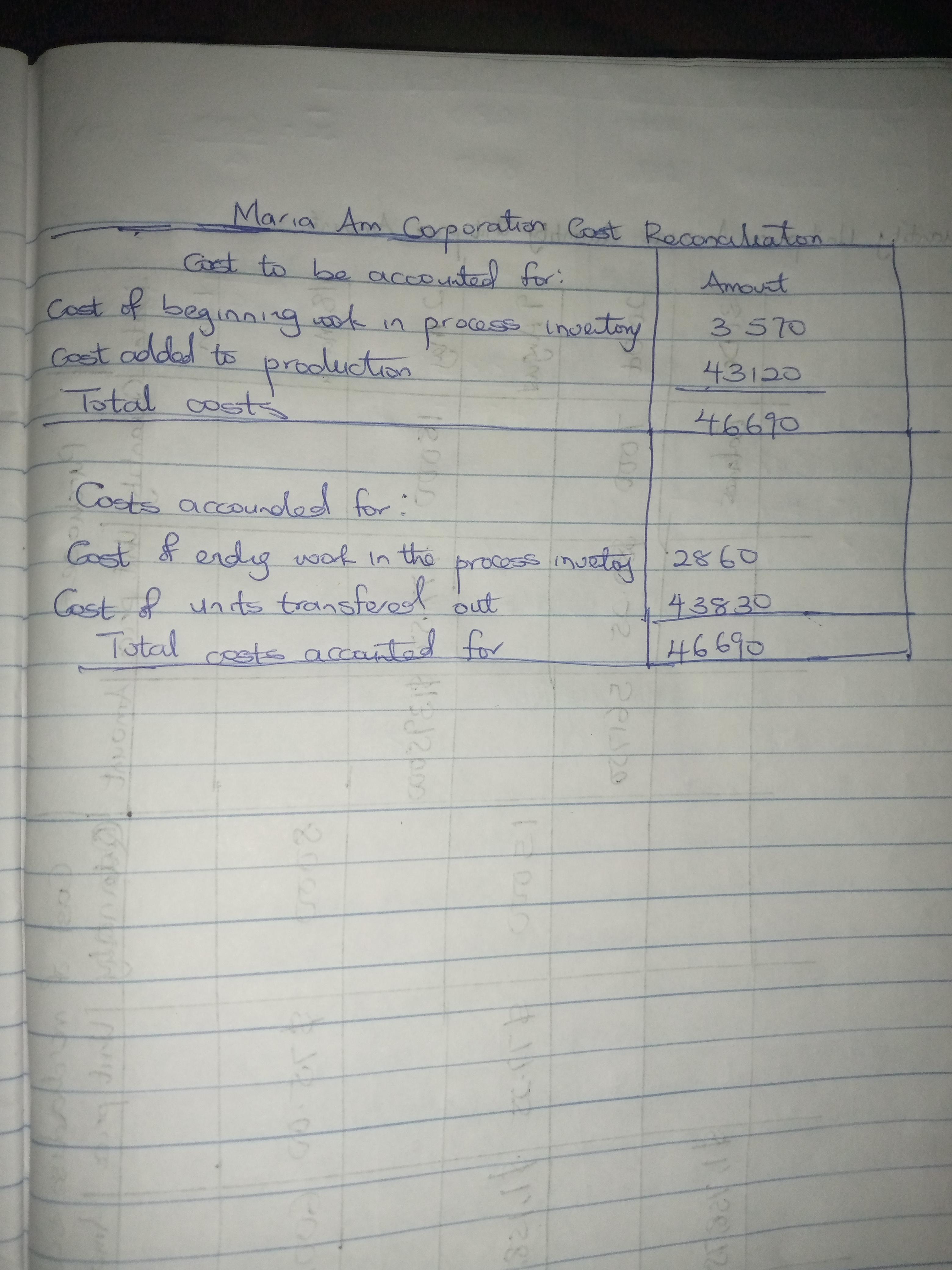

Answer:

Explanation:

The following information can be derived from the question above:

The cost of the beginning work in the process inventory = $3,570

The cost of the ending work in the process inventory = $2,860

The cost that is added to the production = $43,120.

In the attached document, it should be noted that the cost of goods that were transferred out was calculated as:

The total cost to be accounted for minus the cost of the ending work in the process inventory. This is:

= 46690 - 2860

= 43830

The cost reconciliation report for the Baking Department for June has been solved and attached.

Answer:

Short term: Try and sell the one pair of cleats that are used.

Med term: Try and sell Two pairs for a lower price like two pairs for $40

Long term: Try and sell all the cleats before you have to leave the store.

Explanation:

I like goals!