D both the factors are affected favorably by any external factors

Answer:

The answer is letter C.

Explanation:

The supply chain members are independent entities.

Because when the members of a supply chain are independent entities, the risks of conflicts related to goals, expectations, are bigger. Each one of them have their own agenda, so that is the main reason.

Advantages:

<span>Current employees already know the rules, regulations and culture of the organisation.Employees have understanding of how the organisation operates and do not need an induction programme.The organisation knows employees and have detailed records from previous supervisorsOffering opportunities to internal employees may boost the morale of the staff members.Allowing employees to move vertically and horizontally within the organisation could reduce the possibility of her looking for another job.A positive image is created in the organisation</span>

Disadvantages:

<span>No new or fresh ideas are brought into the organisationThe job advertised may require skills not currently available within the organisationPromotion of an internal employee could cause resentment amongst other employees, who may feel they deserve the post more than the promoted employee.The number of applicants from which to choose may be too high or limited.It is possible to promote less qualified employees than those from outside of the organisation, in order to comply with the internal recruitment policy or the Employment Equity Act.Most internal applicants have been stagnant in their posts for so long and will not positively contribute any new ideas.Harden negative attitudes of internal employees cannot be changed by promotion.Lazy employees cannot suddenly change into ‘star’ employees because they have been promoted.<span>Contagious negative habits and behaviour by one negative employee can easily be passed on to other divisions.

</span></span>

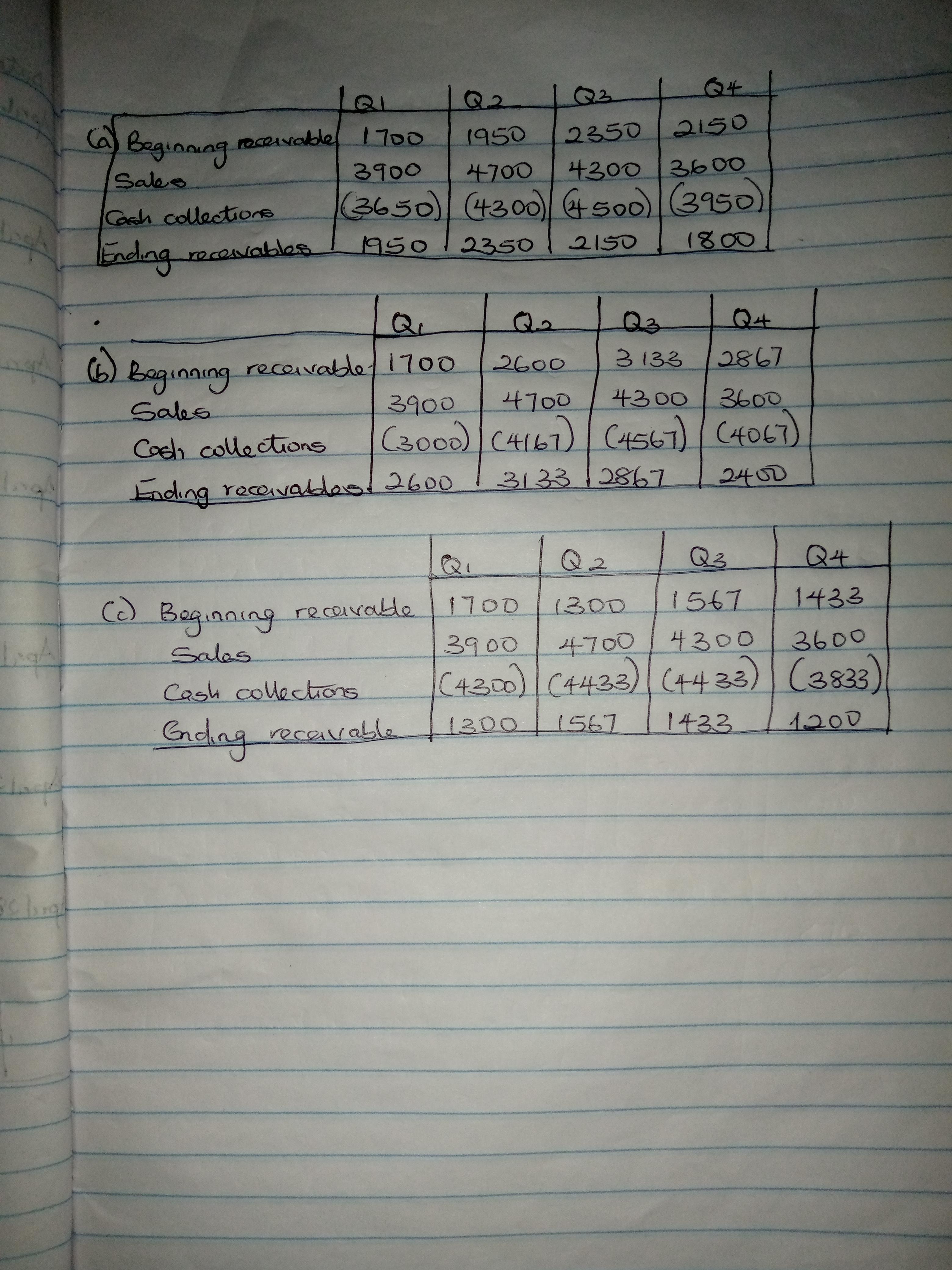

Answer: Check attachment

Explanation:

The cash collection was calculated as:

a. (90-45)/90 = 1/2

Q1 = 1700 + (1/2 × 3900)

= 1700 + 1950

= 3650

Q2 = 1950 + (1/2 × 4700)

= 1950 + 2350

= 4300

Q3 = 2350 + (1/2 × 4300)

= 2350 + 2150

= 4500

Q4 = 2150 + (1/2 × 3600)

= 2150 + 1800

= 3950

Check the attachments for further information.

Answer:

Here are several organization involvements that exist in international trades but might not exist in domestic trade:

- Import/export

- Countertrade Agreement

- Foreign Direct investment

- Multinational marketing strategy

Explanation:

- Import/export

To put it simply, Import is the act of acquiring goods from another country to your country. Export is the act of sending goods from your country to another country,

- Countertrade Agreement

This consist of tradge agreements that created by the government between different countries.

Most countries will impose tariff or quota to the foreign goods that come into their country. This will increase the price of the foreign goods when they entered the local markets. Tariff and quota are made to protect local businesses from foreign businesses.

- Global outsourcing

This happens when a company give their job to the people from another country.

Most commonly, this is conducted by companies from a richer countries. Outsourcing their jobs to a poorer country tend to cut down the labor cost. They can send the product output back to their original country and sell it with higher price/.

- Multinational marketing strategy

This marketing strategy considers the different cultures / taste that exist in foreign market. They will cater their strategy to suit the taste of foreign customers and improve their brand favorability.