Answer:

hello and i am only putting this because i have to complete this

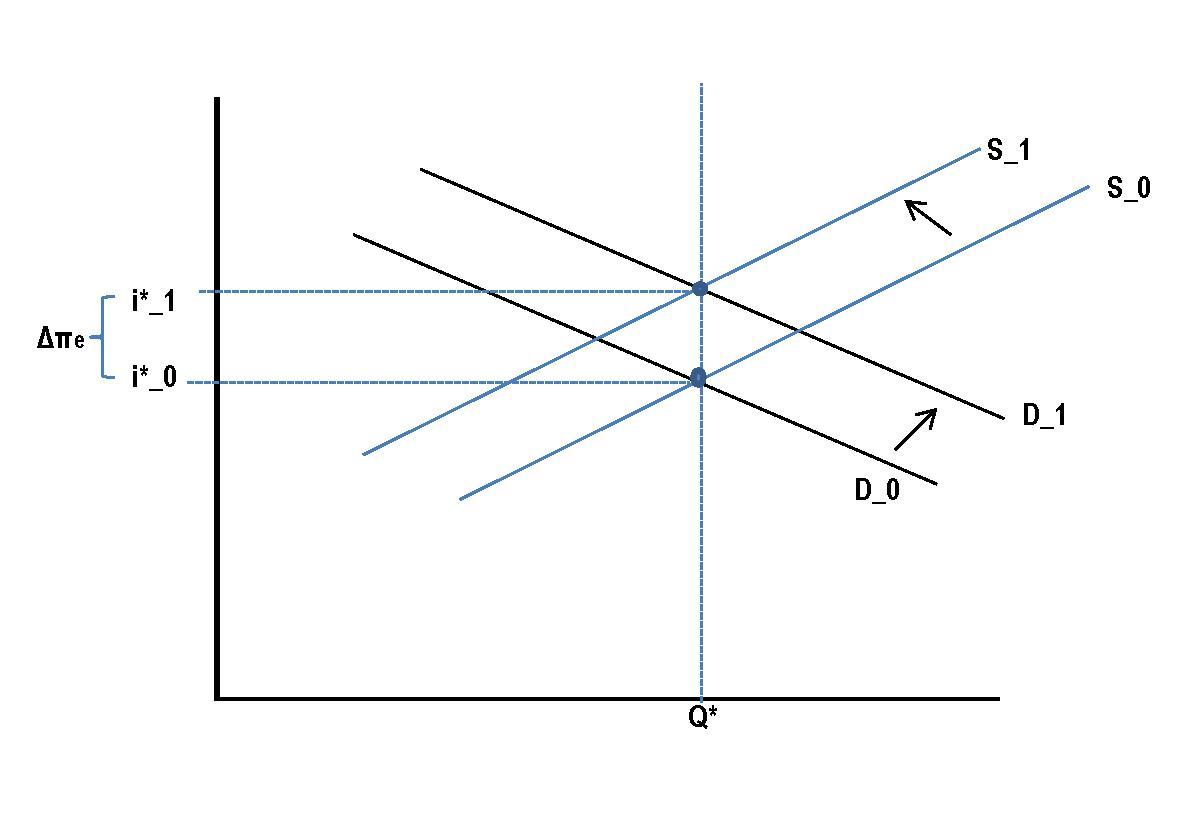

Answer:

shift demand and supply for loanable funds to the right (up), increasing interest rates.

Explanation:

According to the Fisher hypothesis when there is an increase in the expected inflation there is an equal increase in nominal interest rates.

As interest rates rise demand and supply for loanable funds will rise. This is illustrated in the attached diagram. Interest rate moves from i0 to i1.

Inflation is a reduction in the purchasing power of money. When inflation increases money regulation agencies reduce supply of money as a way to reduce price increase. This in turn reduces the amount of loanable funds commercial banks have to give out

I would say that this note would still be valid despite no date on it since it states that it will be paid after the sale of his automobile and in the absence of a date, I believe it could be considered be paid up to 6 months after the sale of the automobile since that sale will have a date or needs to be ensured that such a date is now recorded. While a full signature is preferable, I believe the initial will suffice since some legal documents say at financial institutions only require an initial and in any case the person who initialled it can be contacted to provide his full signature and confirmation that the 6 months after the sale of the automobile can be used.

would reduce the multiplier. If the Fed wanted to offset the effect of this on the size of the money supply, it could have bought bonds

Answer: Option D.

<u>Explanation:</u>

The situation that has been explained in the question would result in the increase in the money in hand with the people because of which the investment decreased and the economy slowed down.

This will have an adverse effect on the multiplier which is working on the economy because of the reduction in the investment in the economy and the fed should work to solve this problem by buying some of the bonds to increase the money in the deposits.

<u />