Answer:

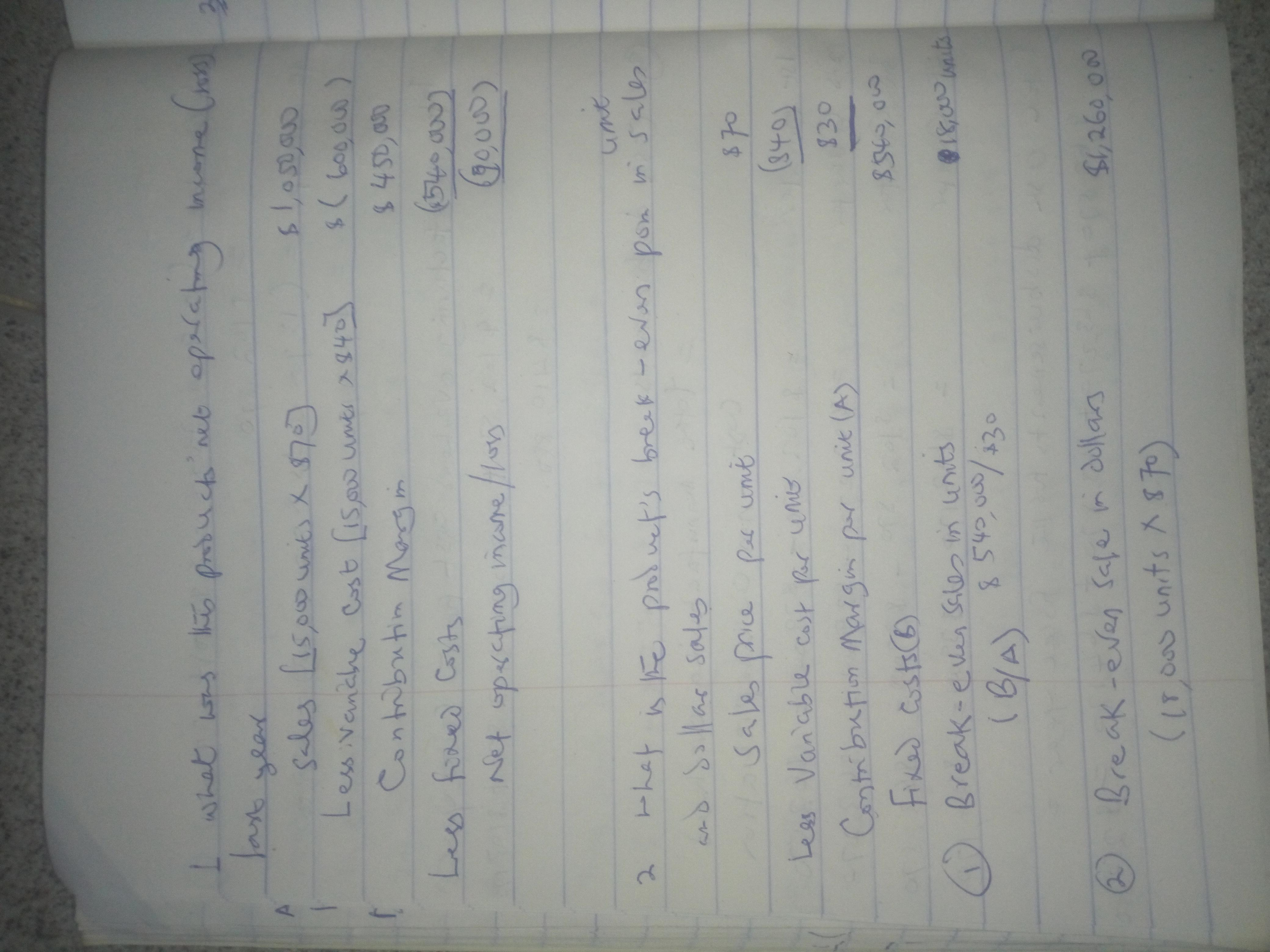

1. What was the product's operating income(loss) last year = $90,000 loss

2. What is the product's Break even point in unit sales and dollars

• Break even sales in units 18,000

• Break even i n sale dollars $1,260,000

3. Maximum annual profit given an increment of 5,000 units and reduction of sales price per unit by $2.

• Net profit of $20,000

4. What would be the break even point in unit sales and dollars using the selling price that you determined in requirement 3.

• Break even sales units 19,285.7

• Break even in sales dollars $1,311,427.6

Explanation:

Please see attached detailed solution to the above questions and answers.

Answer:

The stock price is $37.16

Explanation:

Dividend Valuation method is used to value the stock price of a company based on the dividend paid, its growth rate and rate of return. The price is calculated by calculating present value of future dividend payment.

Formula to calculate the value of stock

Price = Dividend / ( Rate or return - growth rate )

Price = $3.27 / ( 12.2% - 3.4% )

Price = $3.27 / 12.2% - 3.4%

Price = $3.27 / 8.8%

Price = $37.16

Answer:

The operating cash flow in this transaction is zero

Explanation:

Please see attachment.

<h3>Inventory Control</h3>

Inventory control is a process of maintaining the right amount of parts and products in stock to avoid shortages, overstocks, and other expensive problems that might arise in the future.

The purpose of inventory control is to reduce the number of slow-selling products that a company purchases and to increase the number of high-selling products that are purchased. As a result, businesses are able to save time and money. This is because they don't have to spend a lot of time and effort reordering goods that they don't really need, or receiving goods they don't actually need. As an additional benefit, these products are not stored in warehouses at all, which means that transportation costs are reduced and space is freed up for fast-moving finished goods, which is a further benefit.

It is critical to understand that using inventory control can help you avoid making rash decisions, as well as avoiding the pain and expense associated with overstocking your shelves. As its name suggests, inventory control helps you maintain control over your inventory level. This helps you make the best use of your resources and avoid product spoilage and obsolescence.

<em>Hope this helps :)</em>

Answer: 10%, fall

Explanation:

Elasticity of demand = % change in Quantity demanded/ % change in price

therefore % change in Quantity demanded

=2 x 5= 10%

ii) fall , this is due to the decrease in demand which is more than the increase in price.