Answer:

1. Total interest rate is $166,790

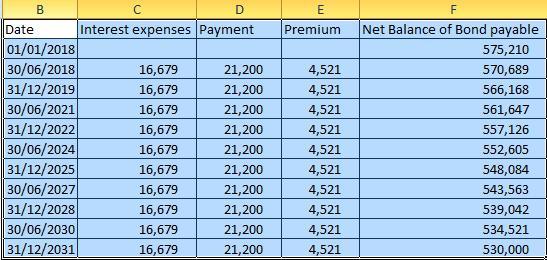

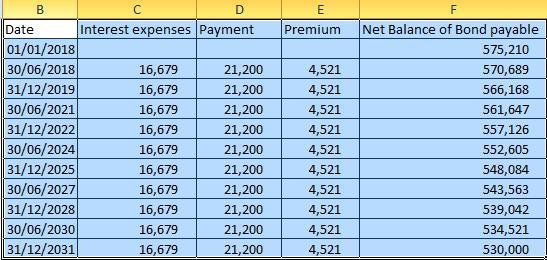

2. Refer to the attached file for the straight-line amortization table for the bonds' life.

3.

To record interest rate paid in 30th June 2018:

Dr Interest expenses 16,679

Dr Premium on bond payable 4,521

Cr Cash 21,200

To record interest rate paid in 31st Dec 2018:

Dr Interest expenses 16,679

Dr Premium on bond payable 4,521

Cr Cash 21,200

Explanation:

Total interest rate as followed : Interest payment - Premium on bond payable = 530,000 x 8% /2 x 10 - (575,210 - 530,000) =166,790.