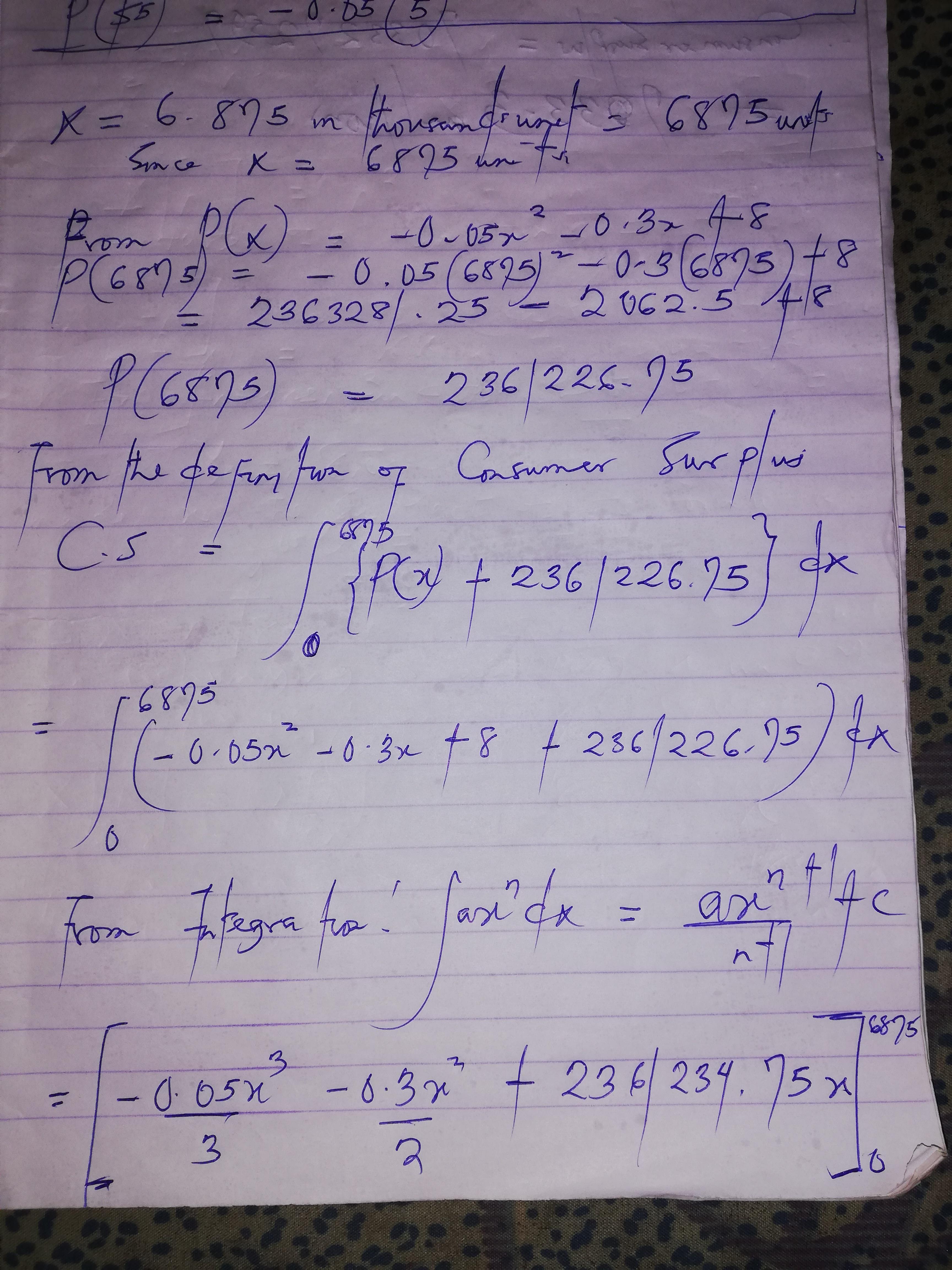

Answer: This is the correct and complete question ; The demand function for a product is given by p = -0.05x2 - 0.3x + 0.8, where p is the unit price in dollars and x is the weekly demand for the product each week, measured in thousands of units. Find the consumer's surplus if the market price for the product is $5.

Answer for the consumer surplus is 7033.3million

Explanation:

The concept of consumer surplus shows the disparity between the price that consumers are willing to pay for a product in the market and the actual price they do pay on a product. Consumer Surplus is also the difference between the price that a consumer is willing to pay for a commodity and the price that the consumer actually pays. For example, if you would pay 76p for a cup of tea, but can buy it for 50p – your consumer surplus is 26p

Consumer surplus is measured as the area below the downward-sloping demand curve, or the amount a consumer is willing to spend for given quantities of a good, and above the actual market price of the good, depicted with a horizontal line drawn between the y-axis and demand curve.

The attached below shows the detailed calculations with steps.

Ranging from a sole proprietorship to a business corporation, a business corporation in the most complex type of business to form. Corporations are for-profit operations formed under the laws of a particular state and regulated by that state, as well as other agencies depending on what the business does.

You expect to find and increase knowledge of what really fits for you to do for the rest of your career life.

Answer:

The correct answer is letter "E": A secondary market transaction.

Explanation:

The secondary market refers to all transactions of securities that happen after the stock's initial offering. It can also refer to the exchanges themselves where these transactions take place. The New York Stock Exchange (<em>NYSE</em>) and the National Association of Securities Dealers Automated Quotation (<em>NASDAQ</em>) are examples of secondary market exchanges.

Companies can implement global marketing by developing a product and promotional strategy that can be implemented worldwide. Global marketing involves the process of devising and conveying a product worldwide with the principal aim of reaching the international marketing community.