Answer:

The correct answer is C.

Explanation:

Giving the following information:

Cash inflows:

Year 1= $11,000

Year 2= $24,000

Year 3= $36,000

To calculate the present value, we need to use the following formula:

FV= PV*(1+i)^n

Isolating PV:

PV= FV/(1+i)^n

Year 1= 11,000/(1.12)= $9,821.43

Year 2= 24,000/(1.12^2)= $19,132.65

Year 3= 36,000/(1.12^3)= $25,624.09

Total= $54,578.17

The scenario that explains when producer surplus is important in the quest for competitive advantage is the economic value creation framework.

<h3>What is economic value creation framework?</h3>

The economic value creation framework is a strategy about the creation of economic value.

Under the economic framework, producer surplus is important in the quest for competitive advantage because this is the profit that a firm captures when producing and selling a good or service.

Learn more about surplus on:

brainly.com/question/380921

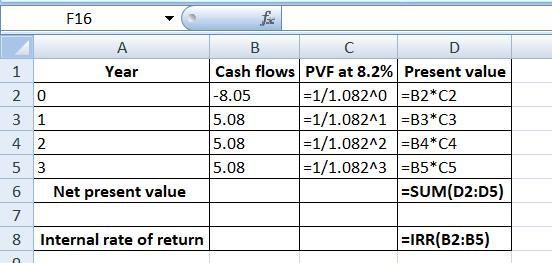

Answer and Explanation:

As per the data given in the question,

($ million) ($ million)

Year Cash flows PVF at 8.2% Present value

0 -8.05 1 -8.05

1 5.08 0.9242 4.70

2 5.08 0.8542 4.34

3 5.08 0.7894 4.01

Net present value 4.99

Internal rate of return 0.40

Net present value = $4.99 million

The project should be accepted

Yes, The IRR rule is agree with NPV.

Please find the attachment for better understanding

Answer:

d. Selling Price

Explanation:

Break even point is calculated as

Thus, break even point in units only in two cases,

- Fixed cost is reduced that is decreased,

- Contribution per unit is increased.

Now, here the options are

a. Increase in units sales volume is of no relevance as will not impact the fixed cost or contribution per unit.

b. Increase in fixed cost will result in higher break even point, as numerator in the fraction will increase.

c. Increase in unit variable cost will ultimately decrease the contribution thus, it is of no relevance.

d. Increase in selling price will increase the contribution per unit, that is the increase in denominator value in fraction, thus, break even units will decrease.

Correct option is

d. Selling Price