Answer: i would say with all the water powered plants i would say electricity is the answer but if its not that then its irrigation or drinking

Answer: Please refer to Explanation

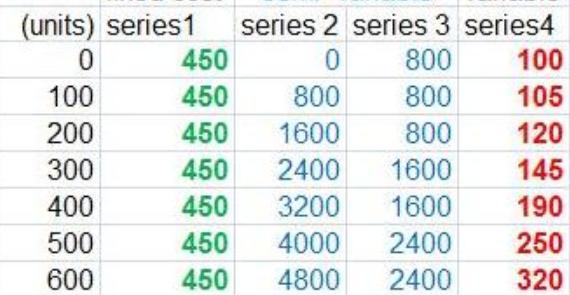

Explanation:

To make your question clearer, I have attached a table that demarcates the figures.

Series 1 are FIXED COSTS. Fixed costs do not change over the production process and are not dependent on the level of production. Even if you were not producing anything you would still be accruing fixed costs. Notice how the cost stays at $450 throughout even when no production was being done. It is a fixed cost.

Series 2 is a VARIABLE COST. Variable costs change as production takes place. They rise as more goods are produced and usually do so at a steady rate. Variable costs are not incurred when production is not going on. Notice in Series 2 how there was no cost at 0 units but as soon as production started the costs started increasing at a steady rate of 800 per hundred units.

Series 3 is what we call STEP-WISE COST. It gets it's name from the fact that it looks like a step when graphed. Why?

These costs stay stable for a certain amount of production and then change depending on if production increases or decreases. Notice how from 0 units to 200 units it stayed the same and then increased and stayed the same again.

I have attached a sample of step wise costs.

Series 4 is what we call CURVILINEAR COST. They are the confused guys so to speak because they increase at an irregular rate as production rises. Notice how it increased by 5 and then by 15 and then by 25. Irregular rate rise. I have also attached a sample of this when it is graphed.

Thanks all I have for today. Thank you for coming to my Ted Talk. If you need any clarification do comment.

Teaming bc when she worked together, they got much more work done.

Answer:

1.the present value for the following assuming that the money can be invested at 11% is $1,209,346.73

2.if she can invest money at 11%, I will recommend that she accept the first option of taking a lump sum of $150000

Explanation:

a) using the compound interest formula

A= p[1+r%]^n

P= $150000 n=20 r=11%

A= 150000[ 1+11/100]^20

A=150000[1.11]^20

A=150000 ×8.062311536

A= $1,209,346.73

2. The first option will give her $1,209,346.73 and the second option will give her ($14,000 ×20)+$60,000= $340000

Therefore the first option is better to accept because she will make more money in the first option than in the second option.

Answer:

c.

Explanation:

Based on the scenario being described it can be said that the action that should be expected to be performed would be connecting multiple processes such as performance management, training and development, and career management. This is because the Integrated Talent Management (TM) approach focuses on all of the HR processes in order to attract, onboard, develop, engage, and retain high-performing employees.