Blah blah blah blah blah blah blah blah blah blah blah blah blah blah blah blah blah blah blah blah blah blah blah blah blah blah

Answer:

variable overhead efficiency variance= $22,780 unfavorable

Explanation:

Giving the following information:

Standard hours per unit of output 7.0 hours

Standard variable overhead rate $ 13.40 per hour

Actual hours 2,725 hours

The actual output of 150 units

To calculate the variable overhead efficiency variance, we need to use the following formula:

variable overhead efficiency variance= (Standard Quantity - Actual Quantity)*Standard rate

Standard quantity= 150*7= 1,050 hours

variable overhead efficiency variance= (1,050 - 2,750)*13.4

variable overhead efficiency variance= $22,780 unfavorable

Answer:

The productivity of the company is $200 per work hour.

Explanation:

Productivity can be measured as the ratio of total output to a single input.

Total output in this case would be value of goods produced, which is 10*10^9 dollars.

Single input in this case would be labour measured in hours of work, which is 50*10^6 hr

Productivity of labor would be: 10*10^9 / (50*10^6) = 0.2*10^3 = $200/hr

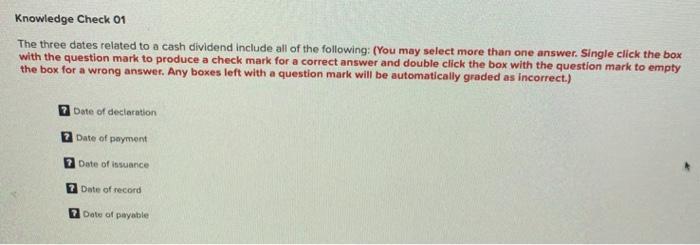

Answer:

Date of declaration, Date of record, Date of payment

Explanation:

Note: The complete question is attached as picture below

The three dates related to a cash dividend include the 3 date below, others are incorrect:

Date of declaration - The date on which directors bind the company to pay the dividend.

Date of record - The date on which recipients are identified.

Date of payment - The date on which cash is paid to stockholders