Answer:

C.

Explanation:

Financial Statements depicts the financial position of a firm at a particular point of time or specified date. The users of financial statements use various types of analysis to understand or compare the current financial statements of the company to prior years or with those of the competitors.

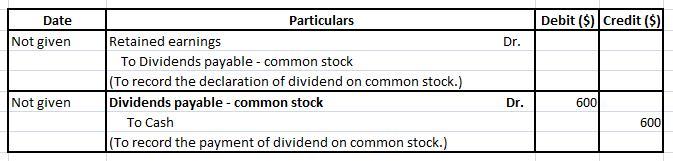

The journal entry on declaration of dividend would lead to a debit to retained earnings and credit to dividends payable.

No journal entry is passed on the date of recording dividend.

Later, on the date of payment of dividend would lead to a debit to dividends payable and credit to cash account.

The journal entries have been shown below:

When CMI International, a composite plastic manufacturer attempt to find and attract qualified applicants from the external labor market for its Community Involvement Office; This process is called "recruitment ".

<h3>What is recruitment?</h3>

The practice of actively seeking out, locating, and employing individuals for a certain post or career is known as recruitment. The entire hiring process, from the first stages to the recruit's integration into the business, is covered by the term of recruitment.

The goal of recruitment is -

- The purpose of recruitment is to build a large pool of qualified candidates from which to select the best candidate for the position.

- This strategy attracts sizable groups of people and motivates them to submit applications for open positions at a company.

Types of recruitment are-

- Direct marketing.

- Databases of the talent pool.

- Worker recommendations.

- Transfers and promotions.

- Exchanges of jobs.

- Recruiting firms.

- Organizations with expertise.

To know more about hiring process, here

brainly.com/question/18859039

#SPJ4

Answer:

D0 = $1.22

Explanation:

Data provided in the question:

Required rate of return, r = 11.50% = 0.115

Selling price of the stock = $29.00

Expected growth rate = 7.00% = 0.07

Now,

Stock price =

here,

D1 is the current dividend

thus,

$29.00 =

or

D1 = $1.305

also,

D0 =

or

D0 =

or

D0 = 1.219 ≈ $1.22

They gain some degree of power by means of differentiating their products from those of other firms in the industry. Remember that a monopolistic competition is the one where many firms selling products that are similar but not identical which is very different from oligopoly and the one known as imperfect competition

<span>The secondary labor market, sometimes called the competitive market, includes low-paying, low-skilled, insecure jobs.

</span>This type of labor market involves high-turnover, low-pay, and usually part-time or temporary work.<span> The secondary labor market mainly consists of high school or college students. </span>