Answer:

Detail Answer is given below

Explanation:

A perceptual map is a graphic used by market researchers and companies to describe and understand how target customers see and feel about a particular brand or product.

Perceptual maps can also be called product positioning maps.

These useful graphics allow organizations to understand the competitive positioning of their brand or product. They also allow organizations to consider comparisons of attributes that are important to customers and identify open areas within their markets.

To obtain the data that is plotted on a perceptual map, surveys are distributed to potential clients and clients who ask them about their experience with a product. These surveys ask about the opinions of respondents about product performance, packaging, price, size and other variables.

Qualitative survey responses are then transferred to a perceptual map using a scale, such as the Likert Scale. The table analysis is used to inform the development and improvement of the product.

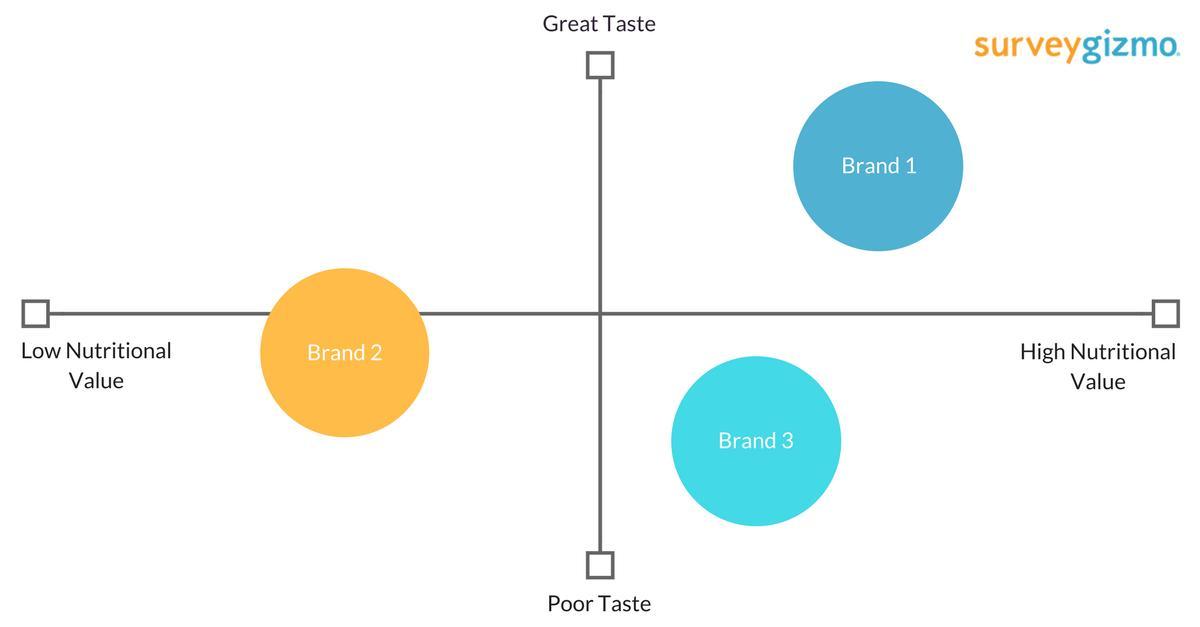

A usual perceptual map is a two-dimensional graph with a vertical axis (Y) and a horizontal axis (X). Respectively axis contains of a pair of opposite attributes at each end.

Format of Map

For example, if the purpose of the map is to investigate how consumers feel about breakfast cereals, the Y axis could have "a great taste" on one end and a "bad taste" on the other. The X axis could have "low nutritional value" at one end and "high nutritional value" at the other end.

Each cereal brand is drawn on the perceptual map based on how consumers perceive the brand's products in relation to those attributes.

For a perceptual map to be as useful as possible, the X and Y axes must measure the attributes that consumers really consider when making purchasing decisions in the real world.

Once again, the best way to begin to understand how customers and potential customers see products and brands in a market is to survey them.