Answer:

a. 25.37% and 13.28%

b. 1.97% and 2.07%

c. Costco

Explanation:

a. The gross margins for Walmart and Costco is shown below:

Gross margin = (Gross profit ÷ revenue) × 100

For Walmart,

= ($126.95 ÷ $500.34) × 100

= 25.37%

For Costco,

= ($17.14 ÷ $129) × 100

= 13.28%

b. The net margins for Walmart and Costco is shown below:

Gross margin = (Net profit ÷ revenue) × 100

For Walmart,

= ($9.86 ÷ $500.34) × 100

= 1.97%

For Costco,

= ($2.68 ÷ $129) × 100

= 2.07%

c. According to the net profit, the Costco has more profitable in 2017

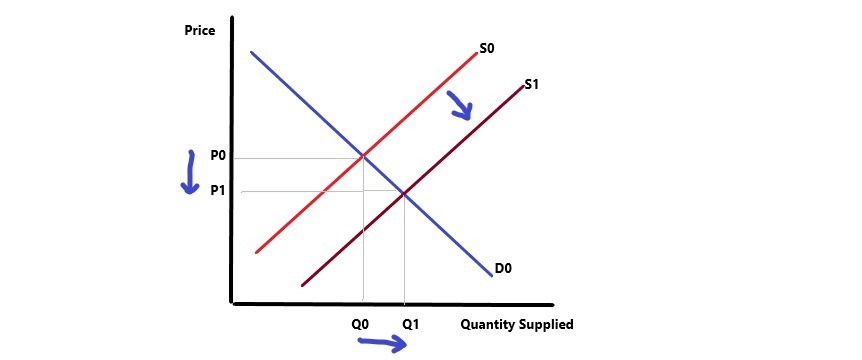

Answer: The price of the product must have declined.

Explanation: If the supply for a product increases the supply curve shifts down to the right. With demand for the product unchanged, this will lead to a decline in the price of the product and an increase in quantity.

As can be seen in the figure, Supply curve shifts from S0 to S1, and price falls from P0 to P1.

Answer:

To achieve its purpose, the Commission's core functions are the following: implement measures to increase market transparency; implement measures to develop public awareness of the provisions of the Act; investigate and evaluate alleged anti-competitive conduct; conduct formal inquiry in respect of the general state of ...

Explanation:

It is a structure which regulates the markets and monopolies in the country. It generally aims in preventing monopoly growth. It benefited by balancing the act of economic transformation that will benefit all South Africans through ownership, the participation of small and medium enterprises and employment.

Answer:

Pitch

Explanation:

Enrico has trouble differentiating between a tuba's sound and a piccolo's sound. Although a piccolo generates sound waves that are much briefer, quicker than a tuba, he has trouble tracking the variations in the pitch of such sounds.

For music, a note's pitch indicates the note's high or low. It is measured for physics in a Hertz unit. A note that vibrates at 261 Hz is induced by pulsing sound waves at 261 times per second.