Answer:

2. Begin with a grid divided into squares.

Explanation:

This is a best approach because it allows for accuracy/precision. To successfully indicate the increase in customer satisfaction on a line chart, before anything else having grid divided into squares makes it easy for her to setup her scale for the two months customer satisfaction data.

After completing this phase, then she could proceed further with the drawing of line chart; which should indicate the rate of change in customer satisfaction on the vertical axis.

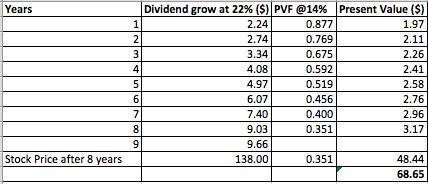

Answer:

Stock price is $68.65

Explanation:

The following image shows the stock price:

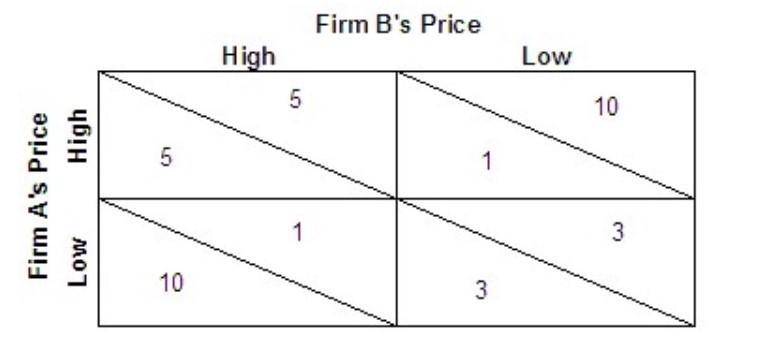

Answer: B. Both firm A and firm B choose the low price.

Explanation:

Both firm A and Firm B will choose the low price and make profits of $3 if there is no cooperation.

This is because at any other price, the other firms could go with the low strategy and get more profit.

For instance, if Firm A is using a low price and Firm B is using a high price then Firm A makes profit of $10 whilst B makes $1.

Conversely, if Firm B charges a low price and A a high price, A will make paltry profits of $1 while B would make $10.

Their best option therefore is to both pick the low price and make $3.

If they were cooperating they could both charge a high price and make $5 each.

Your question was incomplete so I attached the payoff matrix.

A temporary organization plan for matter to be attending .it is used businesses management company