Answer:

$15960.94 is the amount I will have in my account after 17 years.

Explanation:

Firstly we are given the present value of the investment that we will be saving so it will be $7250. we are further given that this investment will be saved during a period of 17 years at different rates through the 17 years so we are looking for the future value after 17 years therefore we will use the future value investment formula as just only one amount is invested.

The future value formula =

where Fv is the future value of the investment after 17 years,

Pv is the invested amount initially $7250

i is the interest rate which here it is 4% for the first 5 years, then 4.6% after for 4 years, thereafter 5.3% for the remaining 8 years so we will.

n is the number of years of the investment as per their given interest rates, substitute these values to the above mentioned formula:

Fv= $7250((1+4%)^5) ((1+4.6%)^4)( (1+5.3%)^8) then compute on a calculator

Fv = $15960.938 then we round off to two decimal places

Fv = $15960.94 which will be the amount that will be saved after 17 years .

A. consumers need to be better informed about what services are available and what those services cost.

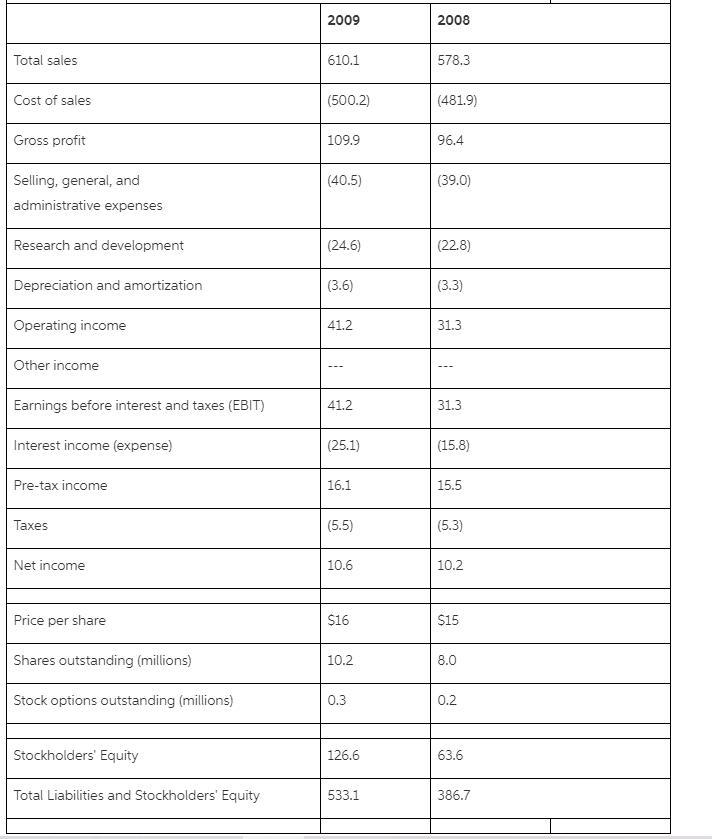

Answer:

2.29%

Explanation:

The computation of the debt to equity ratio using book value of equity is as follows;

As we know that

Debt to Equity Ratio = Debt ÷ Equity

where,

Debt = $239.7 + $10.7 + $39.9

= $2901.1

And, equity is $126.6

Now

Debt to Equity Ratio is

= $290.1 ÷ 126.6

= 2.29%