Psychologists usually attempt to determine whether or not data supports a hypothesis through the use of statistics which means gathering/collecting all data facts and important information.

Explanation:

Ethical awareness means knowing the activities done in personal life or in business dealing. for example incorporating of New Business without aware of the product advantages or disadvantages to the society.Say for example a manufacturing industries of Chemical without knowing its side effects over the environment,animals and on man, if hazardous gas leak outside.

Moral judgement in business is very important as it indicates the decision taken by manager,firm, or any one in the organisation on behalf of the other is affect to the whole group.Whether the decision is right or wrong or doesn't affect the entire group negatively. example Giving salary less than in mentioned papers is not doing right thing to the personnel which is against company morals. Moral characters are the individuals who is judged by his or her consistent qualities.

Answer:

Needs : Frappuccino before work each day and winter coat

Wants: monthly loan payment and paying extra on the principal loan amount

Saving: rent on your apartment

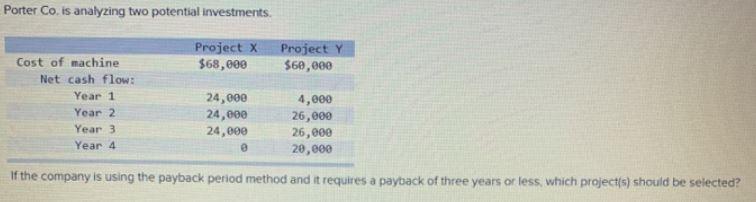

Answer: Project X

Explanation:

The Payback period is the amount of time it would take for the cash inflows accruing from an investment to payoff the cost of the investment.

Project X has a constant cashflow of $24,000 for 3 years and a cost of $68,000 for the Payback period is;

= 68,000/24,000

= 2.83 years

Project Y has an uneven cash flow with a cost of $60,000. Payback is calculated as;

= Year before payback + Amount left to be paid/cashflow in year of payback

Year before payback = 4,000 + 26,000 + 26,000

= $56,000

This means that the third year is the year before payback.

60,000 - 56,000 = $4,000

Payback period = 3 + 4,000/20,000

= 3.2 years

Based on a Payback period of 3 years, only Project X should be chosen as it pays back in less than 3 years.

Answer:

Option A. It will lower its costs through economies of scale.

Explanation:

The reason is that the sales of both of the companies will increase and cost can be controlled by integration of departments like finance department, distribution department, etc. This will decrease the cost of the product which will be because of higher sales and cost benefits due to integration of department and this higher sales increases the production which reduces the cost. So the option A is correct.