Answer:

Statement # 1: False

Statement # 2: True

Statement # 3: False

Statement # 4: True

Explanation:

Lets look at each statement provided in the question and determine which of them is true or false.

Statement # 1 is false. First things first, the interest on this loan amount is higher which is at 4.15%. This is compared to the interest of 4% applicable on loan option 1. Secondly, there is a four year interest only option. This means that for 4 years there will be no repayments of the principal amount which means that the interest of 4.15% will continue to apply on the entire loan amount for these 4 years. In loan 1 however, principal repayments will reduce the principal amount after the 1st year which would further reduce the interest payment in the second year.

Statement # 2 is true. Loan 2 has an interest only period for the first 4 years. During this year you will only pay the 4.15% interest whereas in loan option 1, you will pay 4% interest AND the principal amount. The effect would offset once principal payments start in loan 2 but it would still mean that payments would be minimized in the first few years.

Statement # 3 is false. One of the advantages of having a loan with an interest free clause is that you can pay it off faster than a conventional loan. Since both the loans are fully amortizing, the principal payments would be different but would both result in the principal being repaid in the full 30 year tenor. Any extra payment that you wish to make would be counted towards principal payment in each loan option. However, for loan 1, the total monthly payments you make would remain the same. For loan 2, the extra payments that you make will continue to lower the monthly payments in way of interest which would allow you to save up more to pay more off in principal. The interest only period will also allow you to arrange extra funds during the IO period and repay the principal further. With loan 1, you will continue to make the same monthly payment until the end.

Statement # 4 is true. A fixed payment is being made each year by way of interest and principal repayments and will remain the same till the loan is fully amortized at maturity. In loan 2 on the other hand, a larger balloon payment will start 4 years later since only interest is paid in the first 4 years. So basically you may lower in the first 4 years and more in the remaining years.

Answer:

$ 1,035.18

Explanation:

The price of the bond can be determined using the pv excel function as below:

=-pv(rate,nper,pmt,fv)

rate is the yield of 7.8%

nper is the number of coupons before the bonds are called which is 6

pmt is the annual coupon i.e face value*coupon rate=$1000*7.2%=$72

fv is the call price in six years' time which is $1099

=-pv(7.8%,6,72,1099)=$ 1,035.18

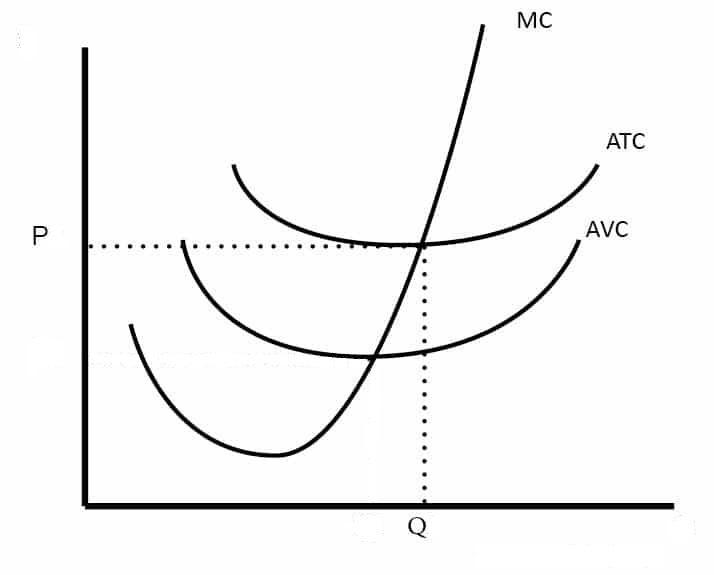

Answer:

U-shaped

Explanation:

Since the marginal product of labor is decreasing, the average variable costs and marginal costs will be increasing at all points, but the average fixed costs will be decreasing. That is why the average total costs (which includes both variable and fixed costs per unit) will be U-shaped since they will fall at the beginning when the decrease in marginal product of labor is small, bu then will increase as the marginal product of labor falls even more.

Currently at the moment the auto brands ford is making is of the following: Lincoln. Have a good day and I hope this helps you :D

Answer: Option B

Explanation: Safeguarding inventory refers to keeping proper records of inventory and protecting it from any kind of damage that may result in loss to the organisation.

The main objective behind safeguarding inventory is to minimize loss of the organisation that is keeping it.

In the given case, second option is the purchase return and it could not be considered a default of the purchaser of inventory.

Hence from the above we can conclude that the correct option is B.