Answer:

First 4 subparts are answered below:

A)

Equation for budget constraint: p1.x1 + p2.x2 = M

Substituting the given information gives: 1B + 5P = 20

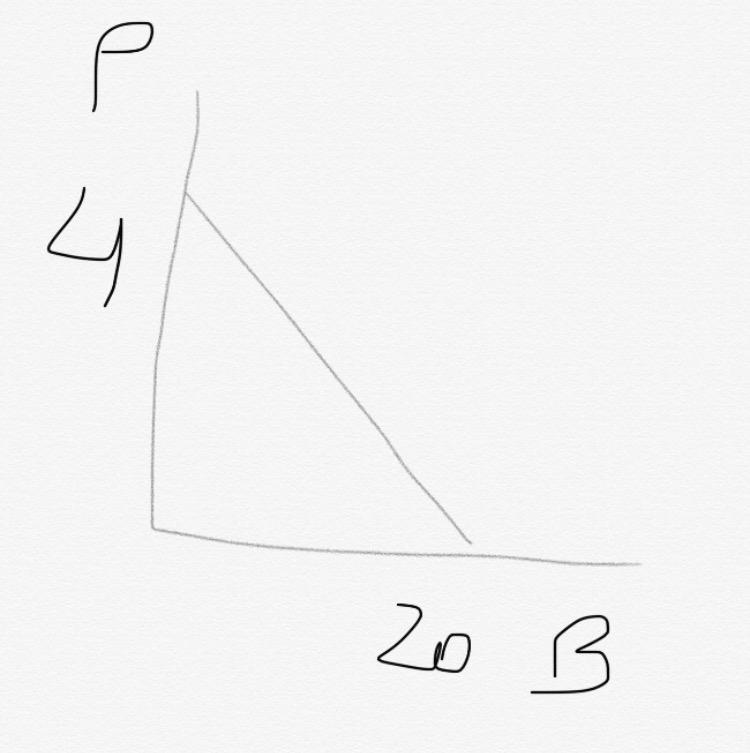

B)

The budget constraint is below: See attachment

C)

Slope of budget constraint: -P(pizza)/P(beer) = -5

D)

New budget constraint: 2B + 5P = 20

New slope: -5/2 = -2.5

New constraint line: See attachment

The answer in the space provided is 'coming from'. It is because the countries like China and India has government which has less over sight which enables them to transport goods from chemical manufacturers because of their government that are not that strict in terms of transporting goods to other countries compared to others countries that have more over sight and are more strict.

Answer:

$1,774.2

Explanation:

Compute the accumulated amount in the account on the date of last deposit'

Formula used to find out the future value ordinary annuity is:

Future value factor of ordinary annuity

1- oily Future value of ordinary annuity

Where:

R = annual return (ordinary annuity)

= future value of an ordinary annuity of I for n periods at i interest

= future value of an ordinary annuity of I for n periods at i interest

Substituting the values:

Future value of ordinary annuity

=

=

Answer:

Normal goods

Explanation:

The computation of the income elasticity of demand is shown below:

Income elasticity is

= (change in quantity ÷ average quantity) ÷ (change in income ÷ average income)

= {(33,000 - 28000) ÷ ((33,000 + 28,000) ÷ 2)} ÷ {($60,000 - $55000) ÷ (($60,000 + $55,000) ÷ 2)}

= (5,000 ÷ 30,500) ÷ ($5,000 ÷ $57,500)

= 0.1639 ÷ 0.0869

= 1.88

As we can see that the income elasticity of demand comes in a positive so it indicates normal goods