Answer:

d. $80 per machine hours

Explanation:

The computation of the overhead rate is shown below:

Overhead rate = Estimated total overhead cost ÷ total machine hours

= $16,000,000 ÷ 200,000 hours

= $80 per machine hours

The overhead rate is come by dividing the estimated total overhead rate by the total machine hours

All the other information that is mentioned is not considered. Hence, ignored it

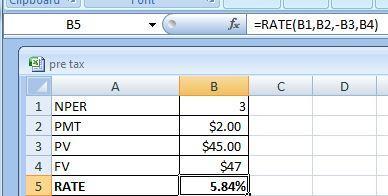

Answer:

5.84%

Explanation:

We use the RATE function that is shown in the excel. Kindly find the attachment below:

The NPER shows the time period.

Given that,

Present value = $45

Future value or Face value = $47

PMT = $2

NPER = 3

The formula is shown below:

= Rate(NPER,PMT,-PV,FV,type)

So, the annual compound rate of return is 5.84%

Answer:

Fraud Investigators Inc.

Date Particulars Debit Credit

31 Mar Accounts Receivable $ 17,000

Service Revenue $ 17000

On March 31, 10 customers were billed for detection services totaling $17,000

31 October Bad Debts $1100 Dr.

Allowance for Doubtful Debts $ 1100 Cr

When Allowance for Doubtful Debts is created .

<em>At the year end this adjusting entry would be passed . This is an adjusting entry and is not passed on 31st October. It is recorded on the year end.</em>

<em> Allowance for Doubtful Debts $ 1100 Dr.</em>

<em> Accounts Receivable $ 1100 Cr</em>

<em />

<em />

Dec 15 Allowance for Doubtful Debts $ 720 Dr

Bad Debts $ 720 Cr

Recovery Of Bad Debts

<em />

Dec 31 Bad debts $ 420 Dr

Allowance for Doubtful Debts $ 420 Cr

On December 31, $420 of bad debts were estimated and recorded for the year

The correct answer is HIGH SCHOOL TEACHER.

A license or a certification is one of the major method that the government used to ensure that the right set of people are employed to do a particular job. Take teaching, nursing and doctoring for instance, these professionals render their services directly to the people and they have great impacts on the people they attending to, sometimes, the way they render their services to their customers determine whether these people will die or live. So, the government has to ensure that qualified and appropriate people are handling these jobs, that is why certificates and licences are needed to do these kinds of jobs.

Answer:

November 1 Inventory 52 units at $79

November 10 Sale 35 units

- COGS = 35 x $79 = $2,765

- Inventory balance = 17 x $79 = $1,343

November 15 Purchase 27 units at $83

November 20 Sale 25 units

- COGS = (17 x $79) + (3 x $83) = $1,592

- Inventory balance = (24 x $83) = $1,992

November 24 Sale 13 units

- COGS = 13 x $83 = $1,079

- Inventory balance = 11 x $83 = $913

November 30 Purchase 39 units at $86

- Inventory balance = $913 + (39 x $86) = $4,267