Answer:

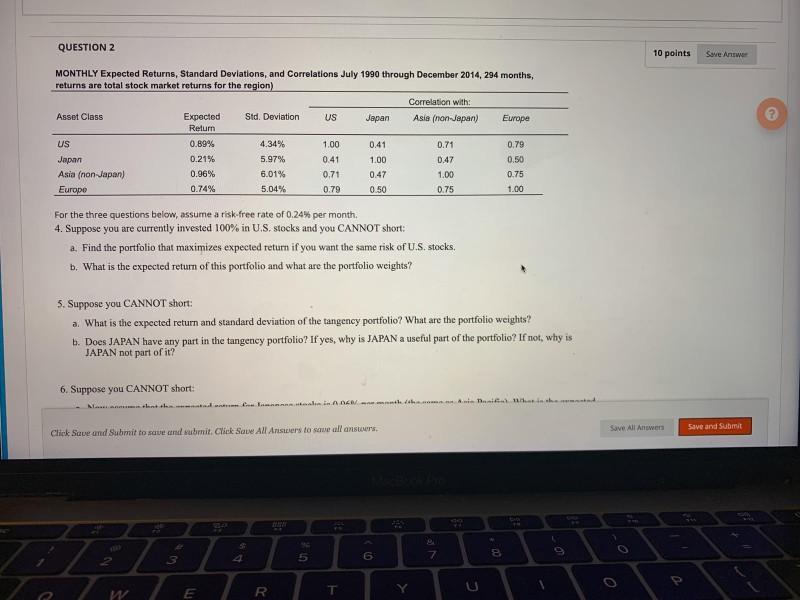

Part a: The portfolio which maximizes the expected return is in the attached file.

Part b:The portfolio's expected rate of return is 11.20% and the weight is 100% for US only.

Explanation:

As the question is incomplete and the data is not available, thus the complete question is found as attached with the solution.

The Sharpe rate is given as

Where

- E_a is the estimated rate of return for a value

- E_r is the risk free rate of return

- σ is the standard deviation of the investment.

The portfolio variance is given as

Where

- σ is the standard deviation of the investment.

- w is the weighted value of the investment

- cv is the covariance term

Portfolio standard deviation is given as

Expected rate is given as

Now the Sharp value is calculated as above.

Now the values as given in the excel sheet are added in the attached excel sheet, following formulas are used to calculate various values

Sharpe ratio is calculated using =(B6-J3)/C6

Portfolio variance is calculated using (=B13^2*C6^2+B14^2*C7^2+B15^2*C8^2+B16^2*C9^2+2*B13*B14*C6*C7*D7+2*B13*B15*C6*C8*D8+2*B13*B16*C6*C9*D9+2*B14*B15*C7*C8*E8+2*B14*B16*C7*C9*E9+2*B15*B16*C8*C9*F9)

Portfolio standard deviation is SQRT(Variance)

Expected return is calculated using =B13*B6+B14*B7+B15*B8+B16*B9

Sharpe is calculated using =(B23-$J$3)/B22

Part a:

The portfolio which maximizes the expected return is in the attached file.

Part b:

The portfolio's expected rate of return is 11.20% and the weight is 100% for US only.