Answer:

The correct answer is option C.your granny's monthly social security payment

Explanation:

Judging from the formula used in computing the GDP,option A relates to household consumption as the new textbook is not for resale.

Option B also points to household consumption expenditure,as the cup of coffee is for household usage.

Option C does not have a place in the formula as it is not a payment for a good or service.It is a payment that cannot be tied to any transaction.Hence,option C is your best bet.

Paying wages means parting with money in return for value-adding services,so it features in the GDP computation.

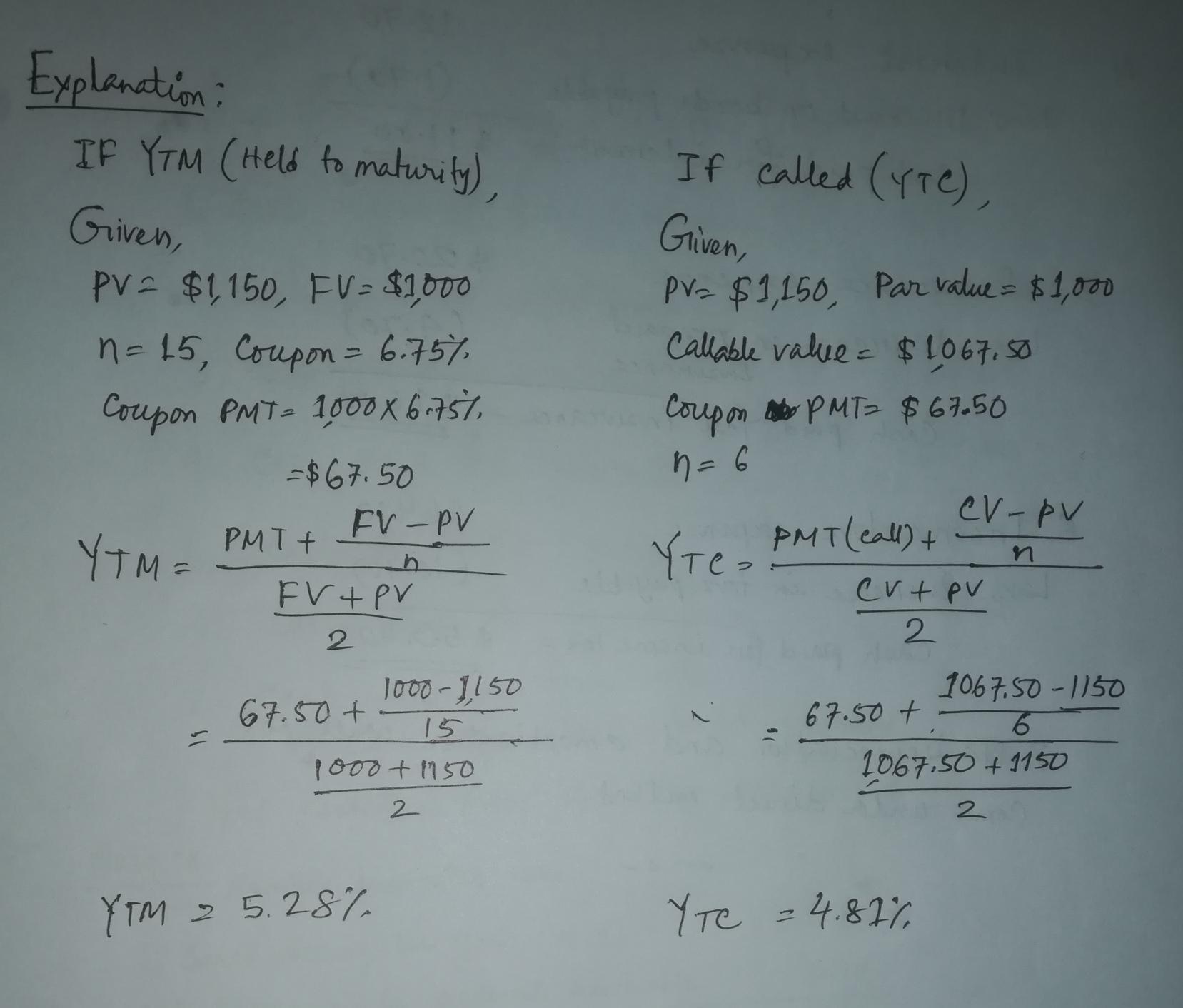

The rate of return should an investor expect to earn if he or she purchases these bonds is 4.81%

<h3>What is

rate of return?</h3>

A return in finance is a profit on an investment. It includes any change in the investment's value and/or cash flows received by the investor, such as interest payments, coupons, cash dividends, stock dividends, or the payoff from a derivative or structured product.

Annual Rate of Return: Definition and Calculation

For example, if an investment is worth $70 at the end of the year and was purchased for $60 at the start of the year, the annual rate of return is 16.66%.

A good return on investment is generally thought to be around 7% per year. Based on the historical average return of the S&P 500 after correcting for inflation, this is the barometer that many investors utilize.

(complete solution in attached image)

To know more about rate of return follow the link:

brainly.com/question/24301559

#SPJ4

Companies and consumers started to understand in the 1930s that using resources properly and efficiently was advantageous for both society and business. the green revolution sprang from this.

The green revolution is a broad movement that advances the concerns of environmentalists, or people who believe that it is important to preserve the integrity of the non-human world for both that reason and the survival of humans. Its membership is extraordinarily diversified, including academics, political activists, wealthy and impoverished individuals from all over the world, as well as followers of a wide range of religious ideologies. Global climate change has been a major issue for the green movement since the 1980s. The preservation of both multi-use undeveloped landscapes and natural regions, the protection of endangered species, and resistance to pollution are further issues.

Learn more about green revolution here

brainly.com/question/25077523

#SPJ4

Answer:

Non-Governmental Organizations or NGOs have become an extensively discussed theme in the third world countries as well vastly in social business world. The NGOs have appeared as the savior of countless number of people without food, cloth, education and basic health facilities. NGOs can continue playing the role of catalyst in the attainment of sustainable economic growth and development provided, an endurable, warm and dependable relationship is there between the government and NGOs where both are working for the benefit of the people with numerable activities. Their main tasks are to organize these people, create awareness in them and make them development oriented. These organizations are working based on the assessed need and demand of the grass root level farmers and women. By involving the beneficiaries of overall national planning for development.

Non-governmental Organizations (NGOs) play an important role in the economic development of developing countries. They provide services to society through welfare works for community development, assistance in national disasters, sustainable system development, and popular movements. They take numerable for actions developing our society. Although agriculture sector is the main source of income for this rural-agro based country, unfortunately this sector has completely failed to create rewarding employment opportunity for the landless. Considering these overall situations, the NGOs are working on poverty eradication by directly involving the poverty stricken population. Their main tasks are to organize these people, create awareness in them and make them development oriented. These organizations are working based on the assessed need and demand of the grass root level farmers and women. By involving the beneficiaries directly, they are working within the context of overall national planning for development.

Explanation:

Answer:

C. Strategic plan

Explanation:

Strategic planning involves developing a business strategy, method of implementing the business strategy and finally evaluating the business strategy in order to see if it has achieve its goal. It is characterized by strategy formulation, implementation and evaluation. In this case, Kia is contributing to the strategic plan by allocating company's resources to meet the long term goals of the company and defining long term activities, that is, developing a business strategy.