Answer:

At least four core functions can be identified.[1] The financial sector should provide the following services:

Value exchange: a way of making payments.

Intermediation: a way of transferring resources between savers and borrowers.

Risk transfer: a means for pricing and allocating certain risks.

Liquidity: a means of converting assets into cash without undue loss of value.

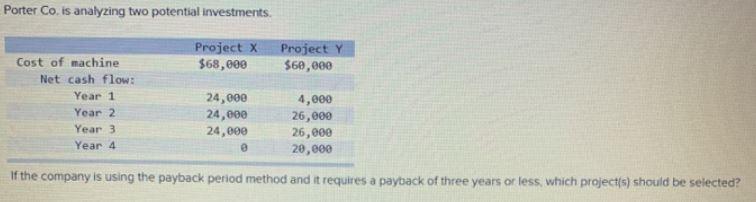

Answer: Project X

Explanation:

The Payback period is the amount of time it would take for the cash inflows accruing from an investment to payoff the cost of the investment.

Project X has a constant cashflow of $24,000 for 3 years and a cost of $68,000 for the Payback period is;

= 68,000/24,000

= 2.83 years

Project Y has an uneven cash flow with a cost of $60,000. Payback is calculated as;

= Year before payback + Amount left to be paid/cashflow in year of payback

Year before payback = 4,000 + 26,000 + 26,000

= $56,000

This means that the third year is the year before payback.

60,000 - 56,000 = $4,000

Payback period = 3 + 4,000/20,000

= 3.2 years

Based on a Payback period of 3 years, only Project X should be chosen as it pays back in less than 3 years.

Still do all the steps of career development starting as soon as possible.

This is true for several reasons. One, even if you plan to stay with the company you can still move up within the company if you network and look for other internal opportunities. Next, you can't predict the future and the company may decide not to hire you after you graduate or decide to offer you a less appealing job so you need to have your career development skills ready to go in case something changes.

Answer:

5% approx

Explanation:

Given that

Number of people in the world = 6.25 billion

And the number of people live in North America = 310 million

So, the percentage of the world population lives in North America would be

= (Number of people live in North America ÷ Number of people in the world) × 100

= (310 million ÷ 6.25 billion) × 100

= 5% approx

The company policy is on communication is an internal communication policy is a record that summarizes an organization's approach to its internal communication with its employees. The internal policy highlights and recognizes what information can be transferred and communicated.

<h3>What are the kinds of workplace communication policies?</h3>

There are four prominent kinds of workplace communication: verbal, body, phone and written. During any point in the workday, you are always encountered with at least one

<h3>Why are communication policies necessary?</h3>

A communication policy can, therefore, be an agency for supporting the periodic planning, development and use of the communication system, and its help and possibilities, and for providing that they function efficiently in enhancing national growth.

To learn more about internal communication, refer

brainly.com/question/5657333

#SPJ9