Answer:

In the context of types of rating errors, Jonathan commits the contrast error.

Explanation:

Contrast error is a concept which involves the rating of an employee according to any other employee. This is an error in which a person is compared with the other and not to any certain standard. In this concept, an individual sets a standard on which the others' work is evaluated. This type of error majorly occurs during interviews and while evaluating the performances for appraisals.

Answer:

$65,000

Explanation:

Computation of the given data are as follows:

Direct material cost = Beginning balance + Purchase - Ending balance

Where, Beginning balance = $37,000

Purchase = $57,000

Ending balance = $29,000

So, by putting the value in the formula, we get

Direct material cost = $37,000 + $57,000 - $29,000

= $65,000

Answer:

to reconsider yourself before spending your emergency funds.

Explanation:

if it's not important then don't use it.

is it unexpected?.. well do you expect to use this fund.

is it necessary?... do you really need this stuff

is it urgent?.... do you need these things right now?

Answer:

Chiquita makes an economic profit of $250,000.

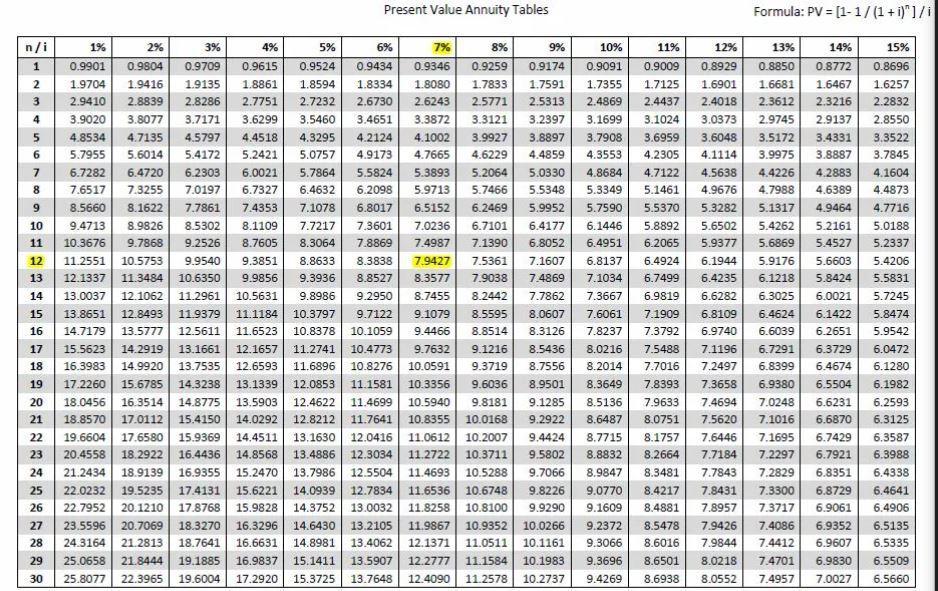

Answer: $80 million per year for 25 years

Explanation:

The option you should choose is one that will guarantee you the highest present value.

This means that you need to discount the annual payment of $80 million per year for 25 years to find the present value. As you did not include a rate, we shall assume a rate of 8% for reference purposes.

The annual payment is an annuity so the present value can be calculated by:

Present value of annuity = Annuity payment * Present value interest factor, rate, no. of years

= 80,000,000 * Present value interest factor, 8%, 25 years

= 80,000,000 * 10.6748

= $853,984,000

<em>The present value of the annual payment is more than the present value of the $850 million received today so the Annual payment should be taken. </em>