Answer:

a. Fuel Interest on company-issued bonds FIXED

b. Shipping charges VARIABLE

c. Payments for raw materials VARIABLE

d. Real estate taxes FIXED

e. Executive salaries FIXED

f. Insurance premiums FIXED

g. Wage payments VARIABLE

h. Depreciation and obsolescence charges FIXED

i. Sales taxes VARIABLE

j. Rental payments on leased office machinery FIXED

Explanation:

Fixed costs are the cost of an organization that don´t change with the amount of production. So , if the production is 0, this cost will exist anyway. For example: real estate taxes, rental

Answer:Telling style leadership

Explanation: According to Hersey and Blanchard’s situational model of leadership, The telling style is an authoritarian type of leadership ususally directed or used with low- maturity followers where the leader gives explicit directions and instructions on how tasks should be performed and orders are not subject to interpretation

This type of leadership usually occurs when the leader has an expertise in the area which he or she specializes and so gives clear, precise quick and controlled instructions for efficient implementation.

Here, Sandra uses the Telling style leadership to accomplish tasks and performances.

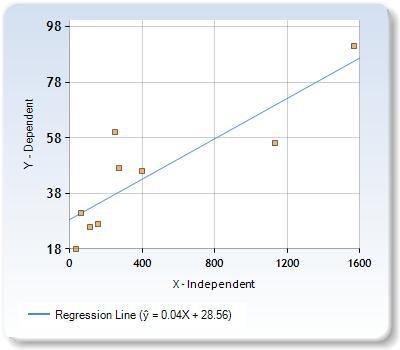

Answer:

H0 : β = 0

H1 : β = 0

R = 0.8642

P value = 0.002654

Explanation:

Null hypothesis : H0 : β = 0

Alternative hypothesis : H1 : β ≠ 0

The correlation Coefficient, R value as obtained using a correlation Coefficient calculator is 0.8642. This depicts that a strong positive relationship exists between court income and Justice salary.

The Pvalue using the Pvalue calculator (R = 0.8642, N = 9) = 0.002654

The Pvalue < α

0.002654< 0.05 ; Hence, we reject H0.