<span>The fact that Ramon funds small businesses that he believes have the potential to grow large and when these companies are still in their initial stages and need investment, he buys their stocks at a low price and later sells them at higher prices when they are successful means that Ramon is a venture capitalist. The term venture capitalist in economics describes a person who i</span>nvests in a business venture, providing capital for start-up or expansion.

Answer:

Option D. management estimates the amount of uncollectibles

Explanation:

When the company estimates the bad debts, reflects it in the balance sheet through a Debit entry in the Bad Debt Expenses againts the asset account Allowance for Doubtful Accounts as a Credit.

When the bad debt are confirm as uncollectible the loss is reflected in the Account Receivable as a Credit with the correspondent debit entry in the Allowance for Doubtful Accounts.

Answer:

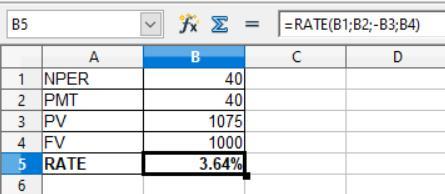

7.28%

Explanation:

For this question we use the RATE formula that is shown in the attachment below:

Provided that

Present value = $1,075

Assuming figure - Future value or Face value = $1,000

PMT = 1,000 × 8% ÷ 2 = $40

NPER = 20 years × 2 = 40 years

The formula is shown below:

= Rate(NPER;PMT;-PV;FV;type)

The present value come in negative

So, after solving this, the coupon rate is

= 3.64% × 2

= 7.28%

Answer:

Depreciation for

2017 = $2,540

2018 = $10,160

Explanation:

Provided, Total cost of the machine = $77,980

Estimated salvage value = $6,860

Therefore, value to be depreciated = $77,980 - $6,860 = $71,120

Total life of asset = 7 years

Depreciation for the year 2017 = October to December = 3 months

Depreciation for the year 2018 =  = $10,160

= $10,160

Under straight line method depreciation is fixed for each year, but in the given case in 2017 the asset is used only for 3 months, thus depreciation will be charged for 3 months only.

Final Answer

Depreciation for

2017 = $2,540

2018 = $10,160

Answer:

d. 1.25

Explanation:

In a business context, the capacity utilization rate is a value that allows the company know how well they are performing compared to what the recorded optimal levels are. In order to calculate this value we simply divide the current operating level for a specific time-period by the optimal level of that same time period, which in this case would be 1 hour. Therefore, in this case we would divide 500 by 400 which would give us 1.25.