Answer:

B. 115

Explanation:

The price index calculates changes in the prices paid by consumers for a basket of goods and services over a period.

Price index = (Cost of basket in a given year / cost of basket in the base year) × 100

230 / 200 = 1.15 × 100 = 115

I hope my answer helps you

<span>Customers' expectations are based on their experiences. if a customer expects his hotel room to be ready when he arrives, but encounters a wait because it is not prepared, this reflects a knowledge gap on the part of the hotel because it did not understand the customer's expectations.

The knowledge gap explains that there are discrepancies that can be made when someone is unsure of another persons expectations. This is common and normal, human error exists. The best thing someone can do moving forward is ask more question to be better prepared but often times, it was not communicated to the appropriate person correctly. </span>

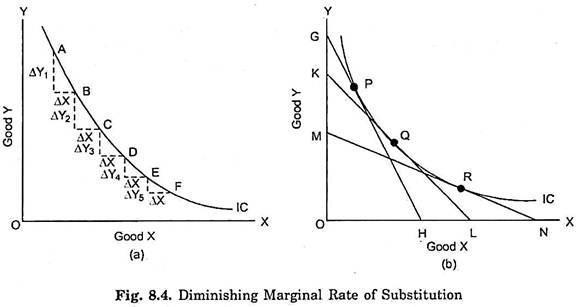

Answer:

diminishing marginal rates of substitution.

Explanation:

Based on the information provided within the question it can be said that the principle that captures this is known as diminishing marginal rates of substitution. Like mentioned in the question this refers to the fact that a consumer chooses to replace a product instead of actually buying more. This decreases as you move down the indifference curve as shown below.

Answer:

C. Sole Proprietorship

Explanation:

Sole Proprietorship is a business owned and less capital required business that can be operated, it is can be operated even by an individual with a simple setup such as a table and a chair in a garage.

With Limited Liability Company (LLC), there are a lot of legal requirements to be reached before setting it up, such as putting in place board of directors, internal auditors and external auditors, mentioning few.

With Partnership it requires two or more individuals in order to operate in addition to a partnership deed.

With Corporation it is similar to the LLC

Thus Sole proprietorship is the simplest and easiest to set up.