Answer:

The Accounting Equation states that;

Assets = Liabilities + Equity

Equity as at 2016 = Assets - Liabilities

= 50 - 13

= $37 million

Equity as at 2017 = Assets - Liabilities

= 77 - 18

= $59 million

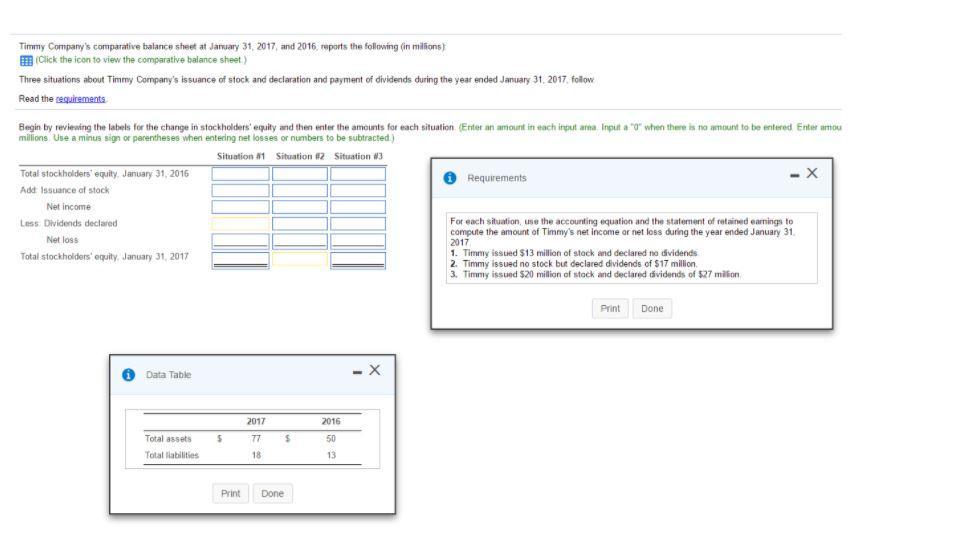

1. Timmy issued $13 million of stock and declared no dividends.

<em>The Net Income ( loss) will be the figure that gives the Statement of Equity a figure of $59 million.</em>

Net Income = Total stockholders' equity, January 31, 2017 - Total stockholders' equity, January 31, 2016 - Issuance of stock

= 59 - 37 - 13

= $9 million

Total stockholders' equity, January 31, 2016 ................ 37

Add: Issuance of stock

......................................................... 13

Net income ......................................................................9

Less: Dividends declared......................................................0

Net loss.......................................................................................0

Total stockholders' equity, January 31, 2017...................59

2. Timmy issued no stock but declared dividends of $17 million.

Net Income (loss) = Total stockholders' equity, January 31, 2017 - Total stockholders' equity, January 31, 2016 + Dividends Declared

= 59 - 37 + 17

= $39 million

Total stockholders' equity, January 31, 2016 ................ 37

Add: Issuance of stock

......................................................... 0

Net income ......................................................................39

Less: Dividends declared......................................................(17)

Net loss.......................................................................................0

Total stockholders' equity, January 31, 2017...................59

3. Timmy issued $20 million of stock and declared dividends of $27 million.

Net Income (loss) = Total stockholders' equity, January 31, 2017 - Total stockholders' equity, January 31, 2016 + Dividends Declared - Issuance of stock

= 59 - 37 + 27 - 20

= $29 million

Total stockholders' equity, January 31, 2016 ................ 37

Add: Issuance of stock

......................................................... 20

Net income ......................................................................29

Less: Dividends declared......................................................(27)

Net loss.......................................................................................0

Total stockholders' equity, January 31, 2017...................59