Answer:

Please see attached solution

Explanation:

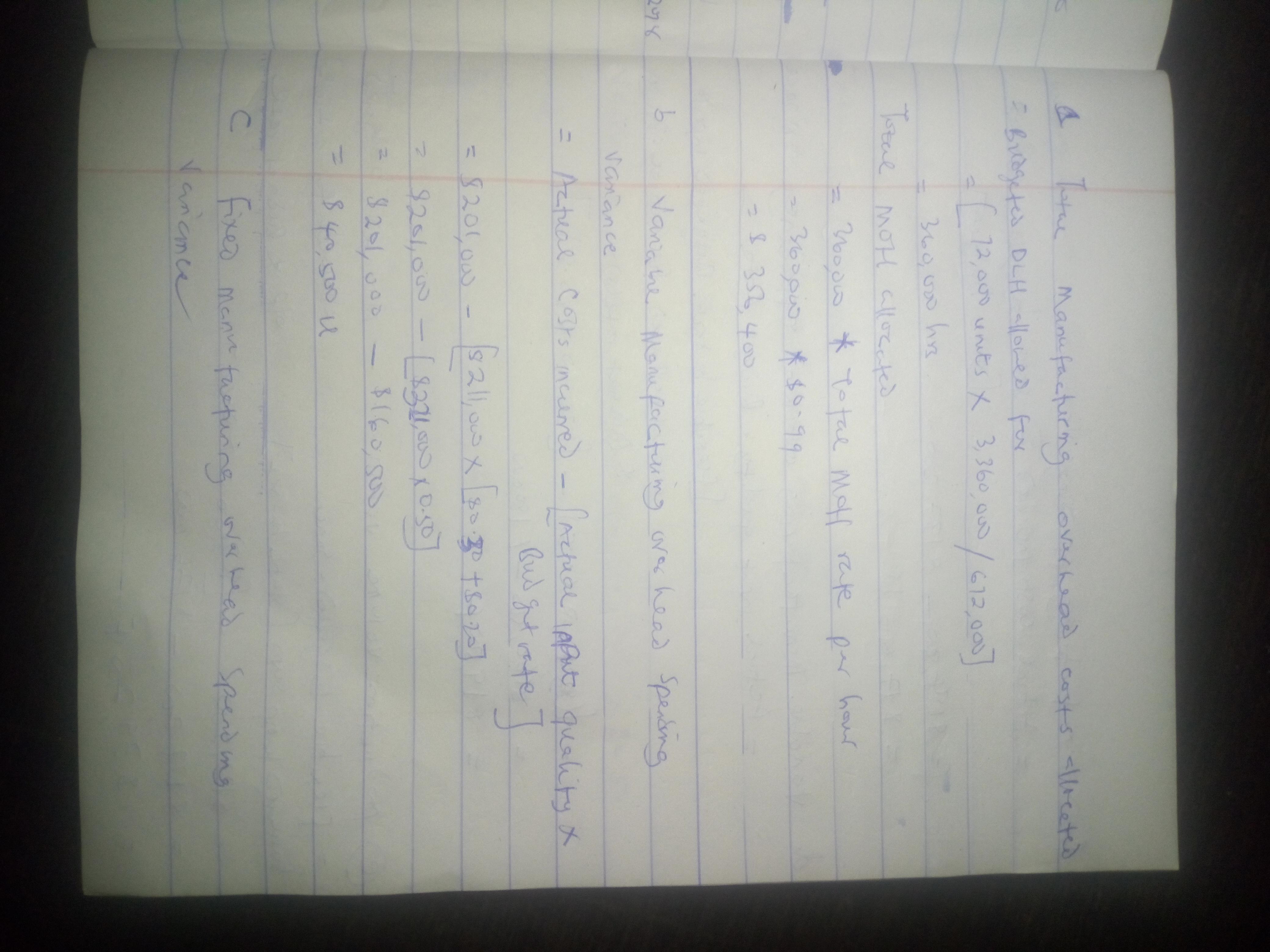

a. Total manufacturing overhead costs allocated $356,400

b. Variable manufacturing overhead spending variance $40,500U

c. Fixed manufacturing overhead spending variance $17,600U

d. Variable manufacturing overhead efficiency variance $19,500F

e. Production volume variance $39,200F

Please find attached detailed solution to the above questions

Answer: A. The company has strong competitive position in its industry and industry growth is sluggish.

Explanation: Diversification is best done from a position of strength, a company should be doing well in its current industry and market before considering diversifying. A company having strong competitive position in its industry and when there is a sluggish growth in that industry, the company can diversified.

Diversification in corporate is a strategy that a company implement to increase market shares and sale volume by introducing new product in another industry and market different from the one they are operating.

Answer:

True, spiff is the actual word

Explanation:

A spiff, or spiv is slang for an immediate bonus for a sale. Typically, spiffs are paid, either by a manufacturer or employer, directly to a salesperson for selling a specific product.

Answer:

D. Land and construction costs are comparatively less expensive in Russia than in Canada

Explanation:

Option D would favor Russia ahead of Canada because of the fact that manufacturing costs are cheaper and they have easier access to Capital. I came to this conclusion since it has been stated that land and construction costs are cheaper in Russia.

In Economics the goal of every firm is to minimize cost and to maximize profit. Option D is cost minimizing for cool cars if they want to duplicate their overall success.