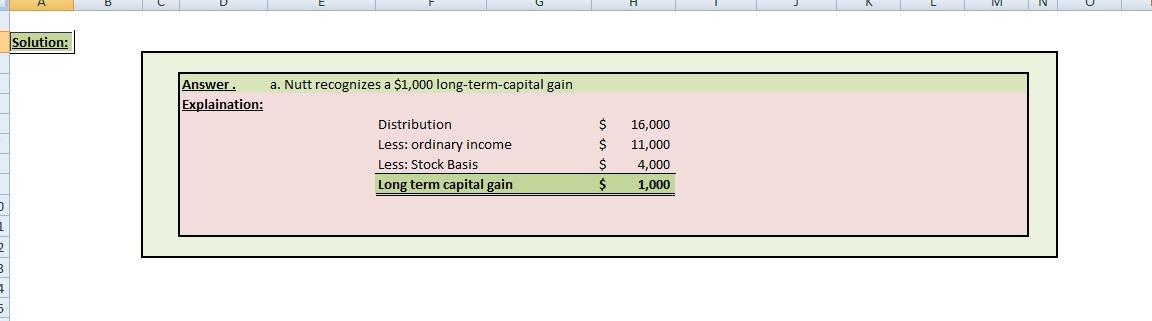

Answer:

Attached image carries the solution to this problem.

Answer: The answer is given below

Explanation:

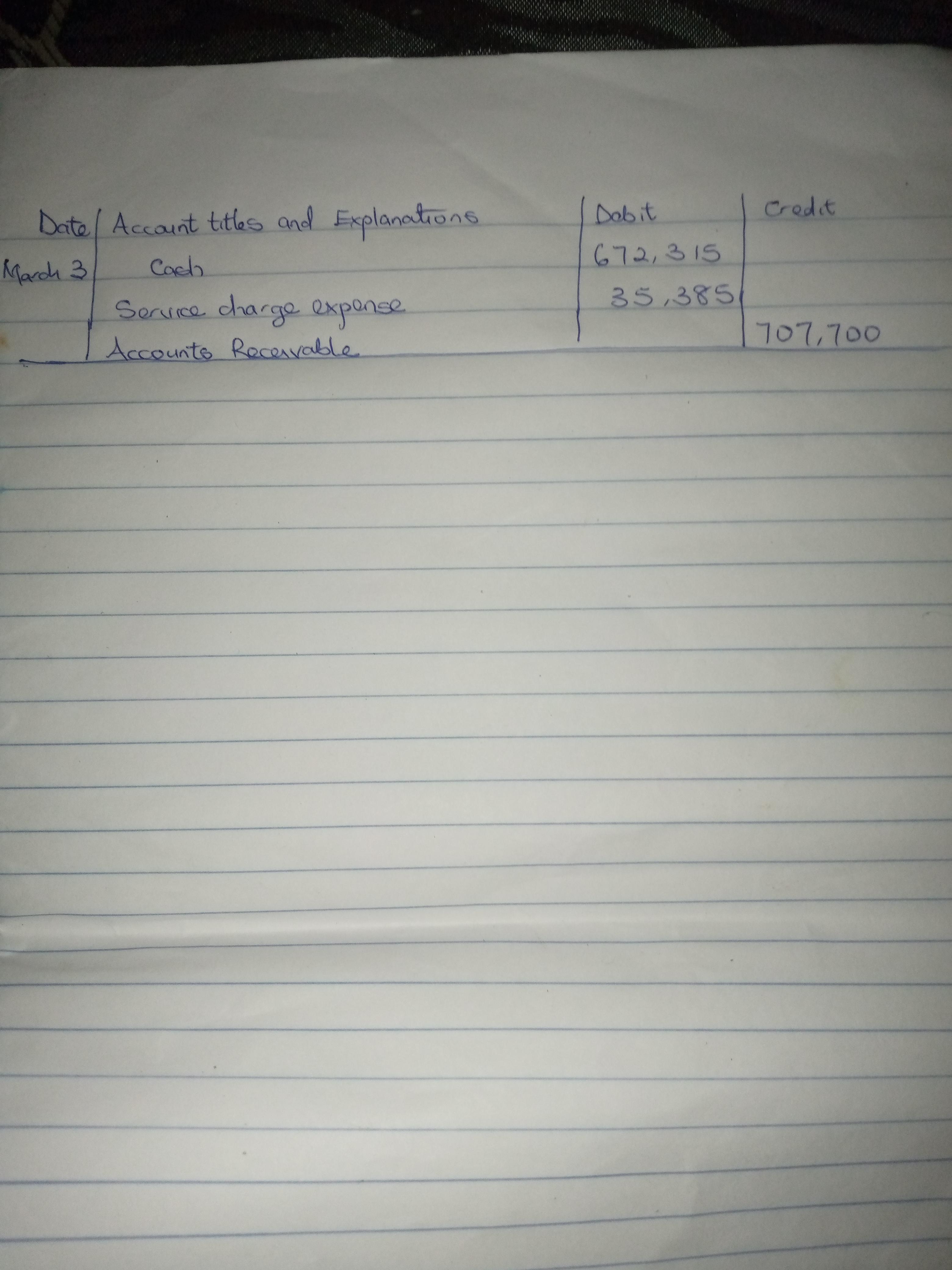

From the question, we are informed that on March 3, Sheridan Company sells $707, 700 of its receivables to National Factors Inc. National Factors Inc. assesses a service charge of its receivables to Western Factors Inc. Western Factors Inc. assesses a service charge of 5% of the amount of receivables sold.

The entry on Sheridan Company books to record the sale of the receivables has been prepared and attached. It should be noted that the service charge expense was calculated as:

= 5% × $707,700

= 0.05 × $707,700

= $35,385.

Other information has been attached.

Answer:

Business markets refer to organizations, businesses, or entities that acquire products and services for use in the production of other services and products. On the other hand, consumer markets refer to markets where producers sell their products or services directly to the final consumers.

Explanation:

Answer:

It will take 1.97 years to payback the machine.

Explanation:

Giving the following information:

It will cost $7,500 to acquire a cotton candy cart. Cart sales are expected to be $3,800 a year for four years.

We need to determine the amount of time required to payback the machine.

Year 1= 3,800 - 7,500= -3,700

Year 2= 3,800 - 3,700= 100

3,700/3,800= 0.97

It will take 1.97 years to payback the machine.

Answer:

i think the answer is true please let me know if it is incorrect

Explanation: