I believe the answer is: A. Federal Communications Commission

The federal communications commissions has the right to regulate interstate communications through television, wire, radio, satellite, and cable. They can give a punishment for companies who conducting an harassment or violation of privacies like mentioned in the case above.

Answer:

The multiple choices are:

$5,589.04

$7,452.05

$4,890.41

$5,876.71

$6,410.96

Amount invested in K is $6,410.96

Explanation:

L+K=12,000

from the return perspective

0.0975=K/12000*0.0805+L/12000*0.117

K=12000-L

Substitute for K in the second equation

0.0975=(12000-L)/12000*0.0805+L/12000*0.117

0.0975=(966-0.0805L)/12000+0.117L/12000

0.0975=(966-0.0805L+0.117L)/12000

12000*0.0975=966+0.0365

L

1170

-966=0.0365L

204=0.0365L

L=204/0.0365

L=$ 5,589.04

K=$12,000-$ 5,589.04

K=$6,410.96

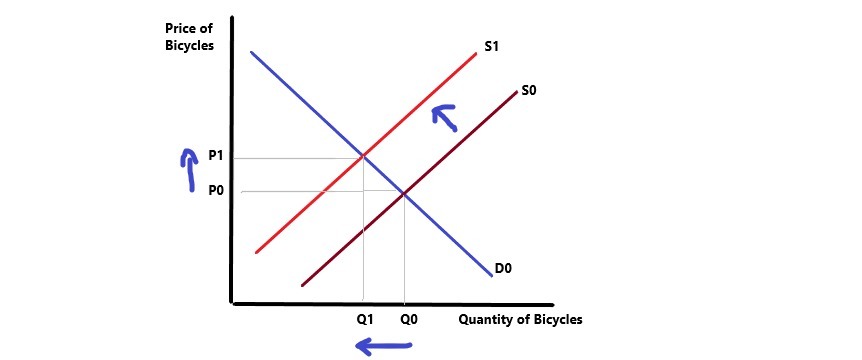

Answer: Higher price of bicycles

Explanation: Higher steel prices will lead to a rise in the input cost of the producers of bicycles. As a result of this, the supply for bicycles will decline shifting the supply curve upward to the left. With no information given about change in the demand for bicycles, the demand curve will not change.

The net effect will be an increase in the price of bicycles.

Answer:

<u>Company's total inventory</u> 30,850

Camaras: 10,960

Camcorders: 8,850

DVDs: 11,040

Explanation:

<u>Camaras: </u>

cost: 10,960

net realizable value: 12,060

<u>Camcorders: </u>

cost: 8,850

net realizable value: 9,170

<u>DVDs: </u>

cost: 12,100

net realizable value: 11,040

<u>Company's total inventory</u>

10,960 + 8,850 + 11,040 = 30,850

We must pick between the historic cost or the net realizable value the lower. The reasoning behind this is the conservatism accounting principle to keep the assets valued at minimum.

Answer:

Quid Pro Quo sexual harassment

Explanation:

Quid Pro Quo means exchanging one thing for another.

Quid pro Quo sexual harassment is a form of harassment in which an employer implies either directly or indirectly that sexual favors will be required, from an employee applying for a job, if he/she is to get the job.

This also applies to employees already within the organization, as it may affect whether they get promoted or fired.