A thesis statement should be clearly stated and narrowly focused. False

Answer:

$100

Explanation:

The computation is shown below;

We know that

Cost of material used = Beginning balance of raw material inventory + purchase made during the month - ending balance of raw material inventory

$900 = Beginning balance of raw material inventory + $1,000 - $200

$900 = Beginning balance of raw material inventory + $800

So, the Beginning balance of raw material inventory would be

= $900 - $800

= $100

Answer:

Red Oak 3,136

Cyril Inc 1,470

Total net revenue 4,606

Explanation:

Red Oak

4,000 - 20% trade-in allowance = 3,200

if payment within discount period: 3,200 x 2% = 64

3,200 - 64 = 3,136 for Red Oak

Cyril Inc

1,500 not qualificable for allowance

payment within discount period

1,500 x 2% = 30

1,500 - 30 = 1,470 for Cyril Inc

Answer:

The revision stage is a step within the writing process. In this stage, the author will review, change or make alterations to their writing. Due to editing a draft, it can sometimes be hard to make changes as you see fit if they aren't major changes that the author can visually see to correct. Sometimes the author gets stuck in making too many or too little changes to their writing.

Explanation:

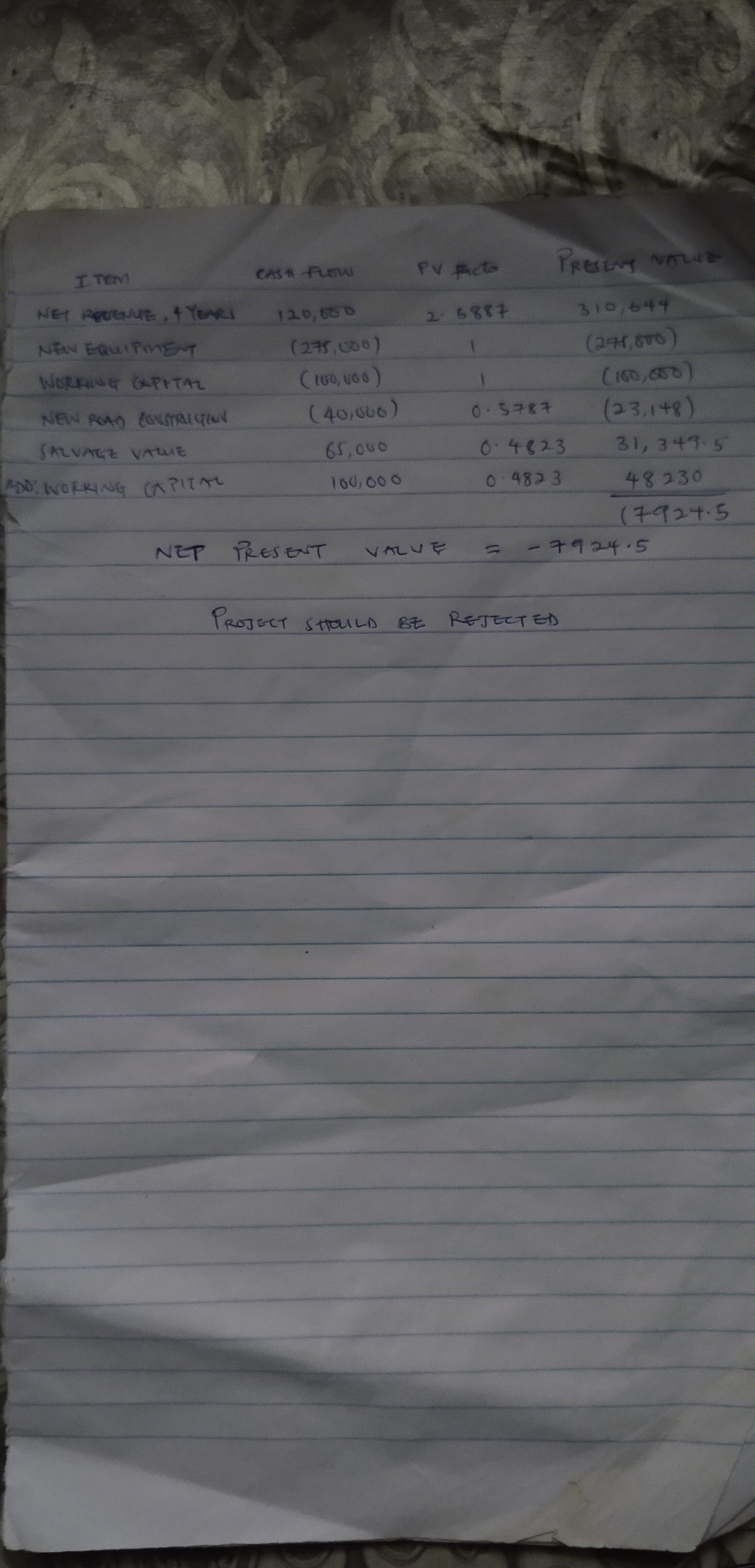

Answer: $7924. 5

Explanation:

Given the following :

Cost of new equipment and timbers - $275,000

Working capital required - $100,000

Annual net cash receipts - $120,000

Cost to construct new roads in year three - $40,000

Salvage value of equipment in four years - $65,000

Kindly check attached picture for Explanation