Answer:

E. Debit Cash $4,000; credit Paid-in Capital in Excess of Par Value, Preferred Stock $1,900, credit Preferred Stock $2,100.

Explanation:

Journal Entry for Issuance of 70 shares of $30 par value preferred stock for $4,000 is -

Cash Debited - $4,000

Paid in Capital in excess of Par value Credited - $1,900

Preferred Stock (70 shares × $30 each) Credited - $2,100

The correct option is - E. Debit Cash $4,000; credit Paid-in Capital in Excess of Par Value, Preferred Stock $1,900, credit Preferred Stock $2,100.

Answer:

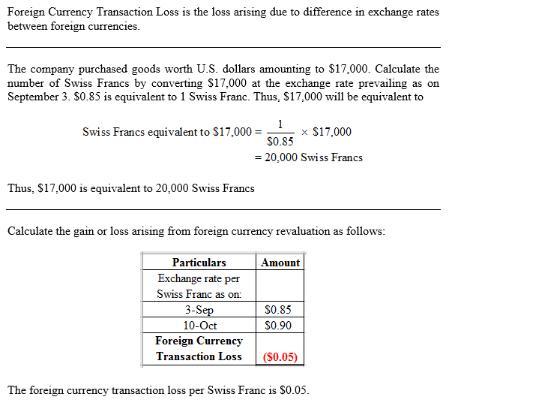

Foreign currency transaction loss : $1000

Account payable : $1000

Explanation:

When Mrs. Watson refuses to hire a person because of their nationality, religion or race is an example of discrimination, also happens when someone treats someone else in a way that is harmful, because of the difference in political ideas, sexual orientation or gender.

Answer:

Organic structure.

Explanation:

Organic structure: It is defined as flat organizational structure as it does not follow normal hierarchical structure, it is more of a decentralized structure with a lesser layer of management at every level, where more information is shared among employee and each department co-operate with other departments, which helps the organization to adapt well with the changes. Employees have the opportunity to participate in the decision-making process of the organization.

In the given case, Steel manufacturing firm are following an environment that is simple and integrated but also dynamic and hostile, which is a perfect organic structure.