Answer:

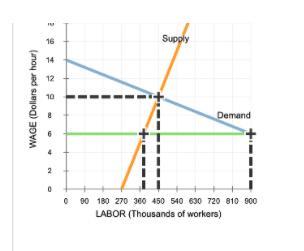

The equilibrium hourly wage is the wage where the curve of supply of labor intersects with that of the demand for labor. The same goes for the equilibrium quantity of labor.

The equilibrium hourly wage is <u>$10</u>, and the equilibrium quantity of labor is <u>450 thousand workers</u>.

If a Senator introduces a minimum hourly wage, this is considered a <u>Price Floor. </u>

Price floors are prices that that the government mandates that one cannot charge below for a good or service. If there is a price floor on cake for instance, a person is not allowed to charge less than that price floor for cake. The Senator's bill is therefore saying that people should not be paid less than $6 an hour.

Boil noodles. add sauce. make meat balls. add it together. yummy.

Answer:

1. c. has no control over the price it pays, or receives,in the market

2. c. firms are at the mercy of market forces.

3. buyers can expect to find consistently low prices and wide availability of the good that they want.

Explanation:

A competitive market has the following characteristics.

1. Firms are price takers. They do not set the price for their goods and services. They accept the price set by market forces. Price is set where the demand curve intersects the supply curve.

2. There are no product differentiation. All sellers sell identical goods and services.

3. There are no barriers to entry or exit of firms in the industry.

4. Firms make zero economic profit in the long run.

5. There are many sellers and buyers.

I hope my answer helps you.

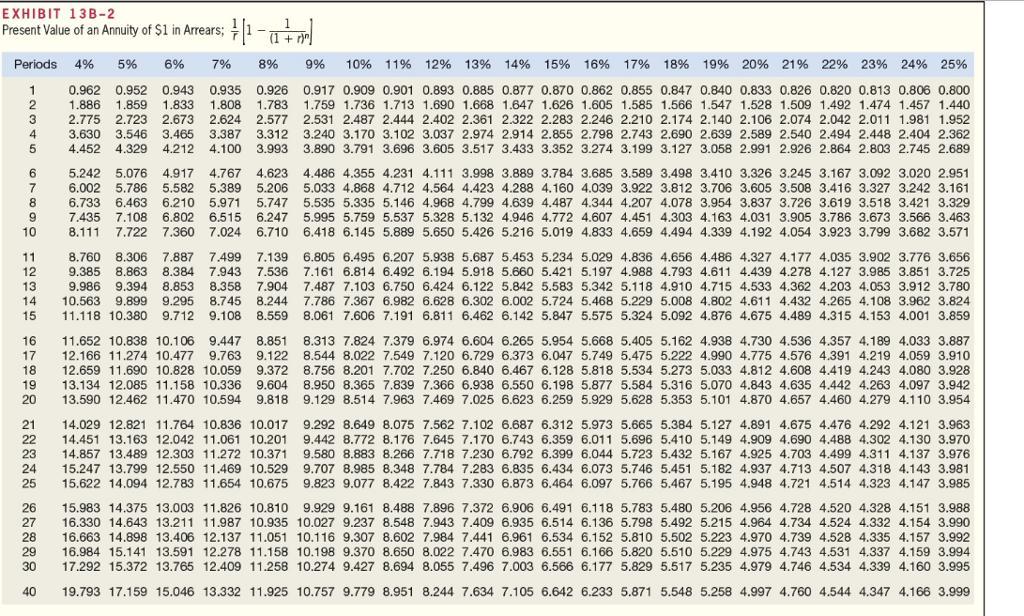

Answer:

12%

Explanation:

initial investment $367,402

net cash flows 1 - 7 = $80,500

the IRR is the interest rate at which NPV = 0

we can calculate it by using Exhibit 13B-2 (present value of annuity in arrears)

$367,402 = $80,500 x present value of 7 year annuity in arrears

- present value of 7 year annuity in arrears at 14% = 4.288

- present value of 7 year annuity in arrears at 12% = 4.564

- present value of 7 year annuity in arrears at 8% = 5.206

with 14% ⇒ $80,500 x 4.288 = $345,184

with 12% ⇒ $80,500 x 4.564 = $367,402 CORRECT ANSWER

with 8% ⇒ $80,500 x 5.206 = $419,083