TD Ameritrade is an example of a brokerage firm, a type of non depository financial institution.

<h3>What are financial institution?</h3>

Financial institution is referred as statutory body which helps in dealing with the financial transactions which includes withdrawing and depositing of money, allowing loans and helping in exchange for the currency.

A brokerage business is a location where stock buyers and sellers can exchange. The company serves as a mediator between buyers and sellers and offers an open trade environment.

This brokerage helps to crack the best deal for their clients. They help to negotiate to get the best resources for business and achieve profit.

Therefore, TD Ameritrade shows the example of brokerage firm.

Learn more about financial institution, here:

brainly.com/question/1122044

#SPJ1

Answer: $1000

Explanation:

You didn't give the options but let me help out.

From the question, we are informed that Hi Phi Unlimited's total revenue from installing 15 sound systems is $30,000 and its total revenue from installing 18 sound systems is $33,000.

The marginal revenue that is received from selling the 18th sound system would be calculated as:

=($33000 - $30000) / (18 - 15)

= $3000 / 3

= ,$1000

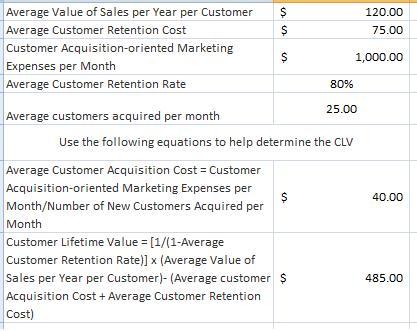

Answer:

Average Customer Retention rate = 80%

Average Value of Sales per year per customer = $120

Average customer acquisition cost = Customer acquisition oriented market expenses per month/

number of new customers acquired per month

Average customer retention cost = $75

CLV =[1/(1- Average customer retention rate)] x (average value of sales per year per customer)-(average customer acquisition cost + average customer retention cost)

![= [1/(1-0.8)] x 120-(40+75)](https://tex.z-dn.net/?f=%3D%20%5B1%2F%281-0.8%29%5D%20x%20120-%2840%2B75%29)

=$485

A) Average customer retention rate =90%

B) Average value of sales per year per customer = $125

C) Average customer acquisition cost =$60

D) Average customer retention cost =$100

CLV = [1/(1- Average customer retention rate)] x (average value of sales per year per customer)-(average customer acquisition cost + average customer retention cost)

![= [1/(1-0.9)] x 125 - (60+100)](https://tex.z-dn.net/?f=%3D%20%5B1%2F%281-0.9%29%5D%20x%20125%20-%20%2860%2B100%29)

E) Customer Lifetime Value = 1090

Explanation:

Here are the spreadsheets.

Answer:

Profit $3,567

I would exercise my option by buying the shares before the expiration .

Explanation:

Calculation of how much profit would you make trading $1,000,000

First step is to multiply the spot rate on the final day by the trading amount

3.4329s*$1,000,000

=$3,432,900

Second step is to divide the spot rate option by the strike price

3,432,900/3.4207

=$1,003,567

Last Step is to find the profit

Profit =$1,003,567-$1,000,000

Profit=$3,567

Therefore the amount of PROFIT you would make trading $1,000,000 will be $3,567

Based on the above calculation I would exercise my option by buying the shares before the expiration .