Answer:

C. What is the relationship between salary, measured in dollars, and age, measured in years?

Explanation:

Qualitative descriptive statistic will provide an enhanced presentation toward a certain occurrence, but the data is not measured by numbers.

When you see option A, frequencies and percentage is measured by numbers. So we can cross this out.

In option D, means and standard deviations is also measured in numbers.

This only leave us with option C.

It allows a fair exchange between labor and being rewarded. Which is also very ethical.

The highest percentage of family income that lenders allow for monthly mortgage payments usually is 36%. This is an example of debt-to-income ratio usage to determine the portion of debt taken by an individual and comparing it with his/her income. The ratio can be obtained by dividing the total debt and the total income of that individual.

Answer:

For 2021, should recognize compensation expense under the fair value method of $170,500

Explanation:

According to the given data we have the following:

option pricing model determines total compensation expense to be $341,000

Also, The option became exercisable on December 31, 2021, after the employee completed two years of service.

Therefore, in order to calculate the amount should recognize compensation expense we would have to make the following calculation:

amount should recognize compensation expense=$341,000/2

amount should recognize compensation expense=$170,500

For 2021, should recognize compensation expense under the fair value method of $170,500

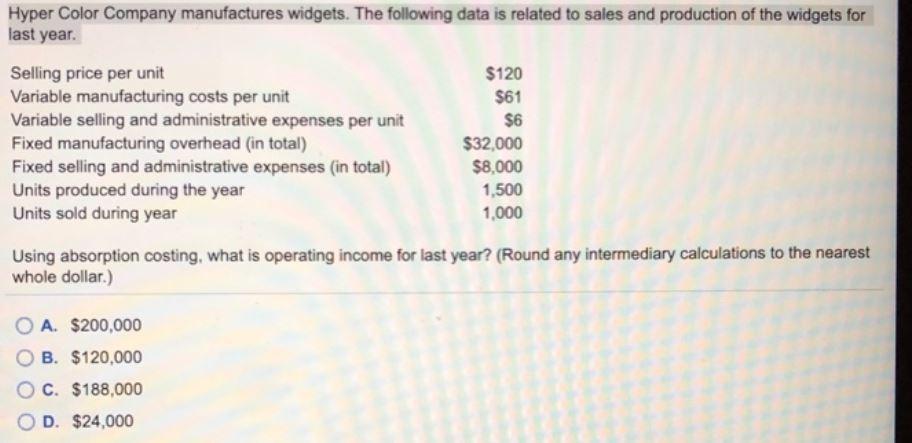

Answer: $24,000

Explanation:

Operating income under absorption costing:

= Sales - Cost of goods sold - Selling and admin expenses

Cost of goods sold = Variable production cost + Fixed production cost

= (61 * 1,000 units sold) + (32,000 / 1,500 units produced * 1,000 units sold)

= $82,333

Selling and admin expenses:

= Variable + Fixed

= (6 * 1,000) + 8,000

= $14,000

Operating income = (120 * 1,000) - 82,333 - 14,000

= $23,667

= $24,000