Explanation:

The preparation of the year-end income statement for Fighting Okra Cooking Services is presented below:

Fighting Okra Cooking Services

Income statement

As on December 31

Revenue

Service revenue $78,500

Total revenues $78,500 (A)

Less: Expenses

Postage expense $1,500

Legal fees expense $2,600

Rent expense $21,000

Salaries expense $22,000

Supplies expense $20,000

Total expenses $67,100 (B)

Net income $11,400 (A- B)

Answer:C. $50,000

Total revenue would be $300,000. Total cost would be $250,000 (fixed = $50,000; variable = $200,000).

Explanation:

Answer:

C) perfectly elastic and identical to the firm in perfect competition.

Explanation:

In a perfectly competitive market, firms supply identical products, so the customers are indifferent towards buying the product from any supplier. What makes a monopolistic competition market different is that products are differentiated, so the customers will choose from which supplier to purchase the product.

When the products are identical (not differentiated), then the firm's demand curve will be perfectly elastic because a change in price will make their customers simply change the supplier. I.e. the products are all substitutes.

Answer:

Cost of goods sold assuming LIFO would be $474

Explanation:

Date Q U.cost Cost Sold Inventory Cost

april 1 530 2,37 1256,1 330 200 474

apri 20 310 2,5 775 310 0 0

640

Answer:

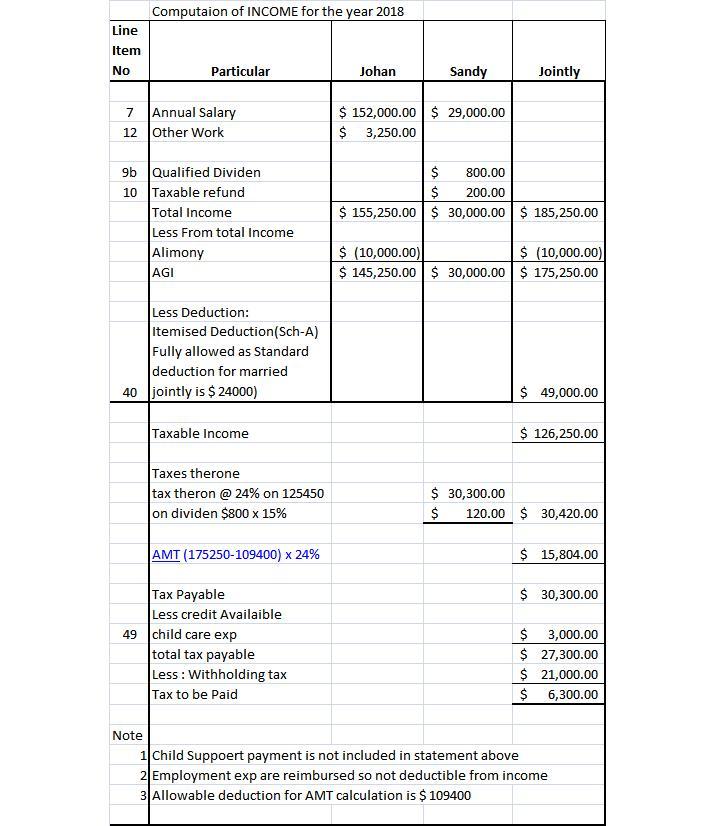

Explanation:

The diagram and step by step solution to the answer can be seen in the attached image below

KINDLY NOTE: Self Employment tax (<u><em>which can be said to be a Medicare tax and Social Security paid by self-employed individuals. It is quite similar to the FICA and usually, they are withheld from an employee’s paycheck Medicare taxes and Social Security purposes.)</em></u> is not applicable to both and the AMT is less then the actual normal tax liability so AMT provision also not applicable.