Answer:

Note: <em>The complete question is attached as picture below</em>

<em />

We are add the previous month +10% to get that month's amounts

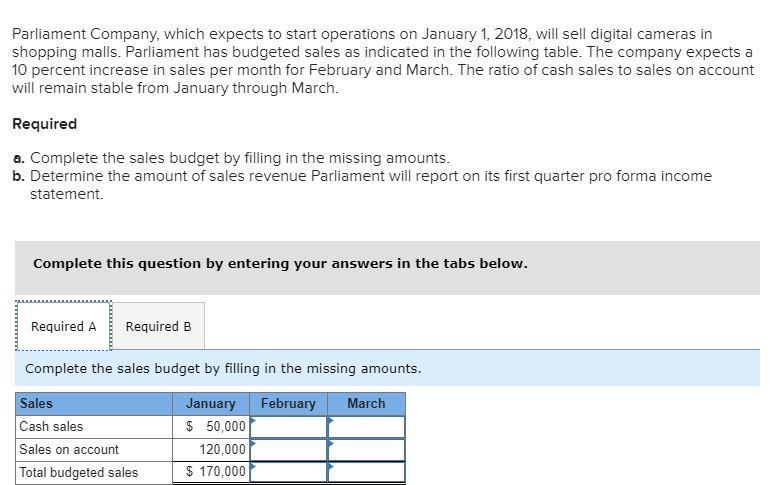

Sales Budget

January February March

Cash sales $50,000 <u>$55,000</u> <u>$60,500</u>

Credit sales $120,000 <u>$132,000</u> <u>$145,200</u>

Total sales $170,000 <u>$187,000</u> <u>$205,700</u>

<u>Workings</u>:

February

Cash sales = 50,000+(50,000*10%) = $55,000

Credit sales= 120,000+(120,000*10%) = $132,000

March

Cash sales = 55,000+(55,000*10%) = $60,500

Credit sales= 132,000+(132,000*10%) = $145,200