Answer:

Details Dec. 31, 2021 Dec. 31, 2022

1. Projected benefit obligation $250 $645

2. Plan assets $260 $556

3. Pension expense $250 $369

4. Net pension asset or net pension liability $10* $89**

Where:

* implies asset

*** implies liability

Note: The figure above are in thousands buy entered as required in the question (Enter your answers in thousands (i.e., 200,000 should be entered as 200).)

Explanation:

Note: See the attached excel file for the calculations Projected benefit obligation, Plan assets, Pension expense, and Net pension asset or net pension liability for December 31, 2021 and December 31, 2022 respectively.

<span>Answer choices are:

</span>a. The loan must have a cosigner

b. Used for vehicle purchases only

c. Fixed initial rate followed by periodic rate adjustments

d. A short duration of a loan, usually five years or less

Correct answer choice is:

c. Fixed initial rate followed by periodic rate adjustments

<span>hybrid ARM loan </span>is a loan that starts with a fixed interest rate for a specific period of time, that can be in few years, and later on, the terms are changed to a variable rate of interest for the remaining amount of time period.

Answer:

uhhhhhhhhhhhhh i guess teacher

Explanation:

<span>Microcredits are usually small which is why they're micro. That's why the correct answer is B. start a small business out of ones home. This is usually a small amount of money, for example, enough to buy a sewing machine and supplies that you need to be a tailor or something similar. The other options often include large sums of money.</span>

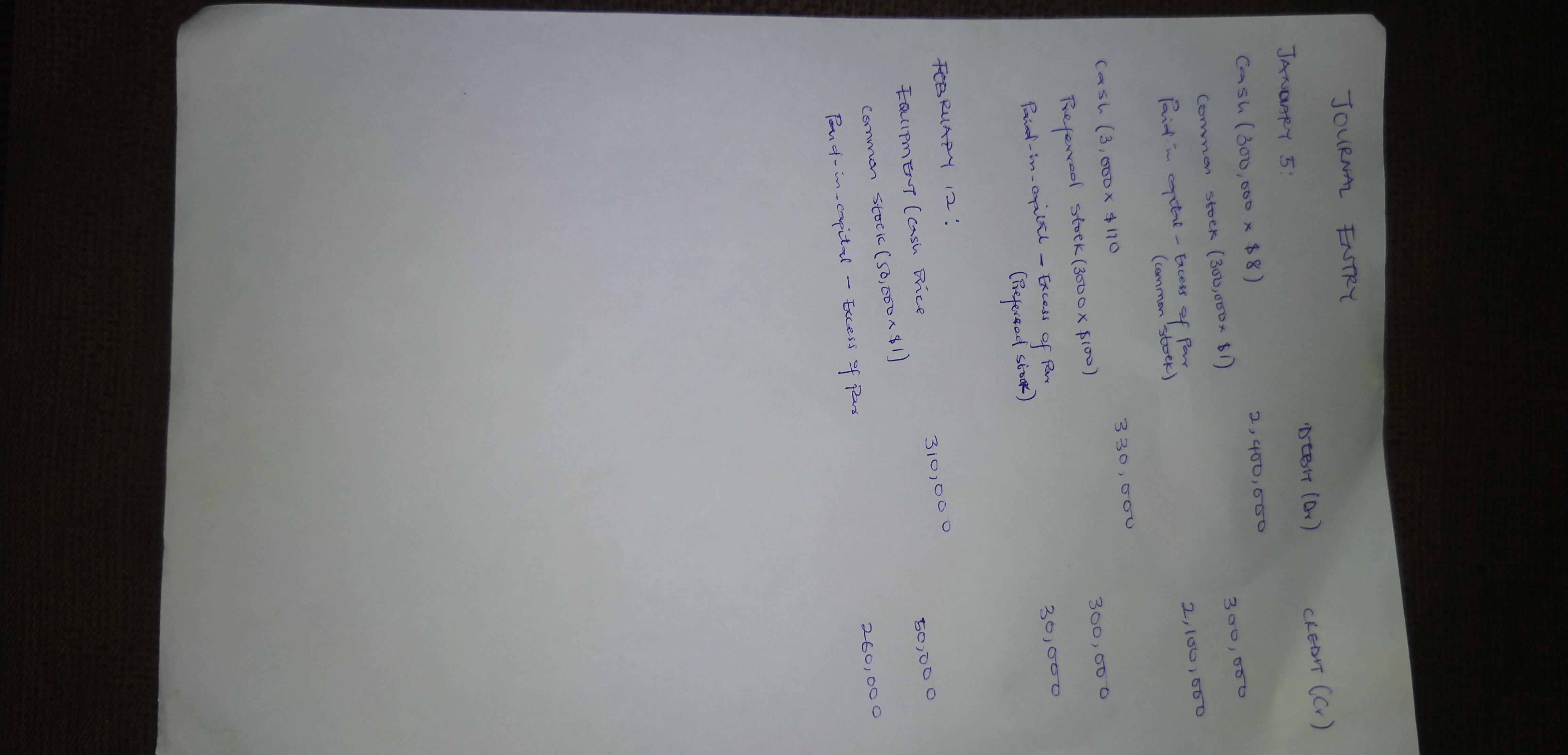

Answer:

Kindly check attached picture for detailed answer and explanation

Explanation:

Given :

January 5: Issued 300,000 of its common shares for $8 per share and 3,000 preferred shares at $110. February 12: Issued 50,000 shares of common stock in exchange for equipment with a known cash price of $310,000. The articles of incorporation authorize 5,000,000 shares with a par value of $1 per share of common and 1,000,000 preferred shares with a par value of $100 per share.