Answer: physical,Mental,Emotional

Explanation:right answer on edgenuity

Answer:

Money available to the buyer is most important factor which needs to be considered. Also the quality of the old tires is considered before making a decision to replace tires. The life of tire is dependent on the running of the car plus the quality of the roads.

Explanation:

The tire are replaced once they are damaged. The damage can be through accident, roughness of roads, extra mileage and other similar factors. Once the tire is damaged it is better to replace it by the new one as this can be harmful for the commuters to travel in a car whose tires are damaged. There can be puncture or even tire burst situation which could be a threat to life.

When interest rates on treasury bills and other financial assets are low, the opportunity cost of holding money is <u>low </u>so the quantity of money demanded will be <u>high</u>.

If interest rates go up, the demand for money will go down. Once it equals the new money supply, there will be no more difference between how much money people are holding and how much they want to keep, and the story is over. This is why (and how) a decline in the money supply raises interest rates.

As interest rates rise, the amount of money demanded decreases because the opportunity cost of holding money decreases. As interest rates rise, aggregate demand shifts to the left. The interest rate effect arises from the idea that higher price levels reduce the real value of household holdings.

Learn more about interest rates here: brainly.com/question/1115815

#SPJ4

Part A:

Given that three firms make up the entire wig manufacturing industry<span>. One has a 50% market share, and the other two

have a 25% market share each. The Herfindahl index of this industry is given by:

</span><span>The Herfindahl-Hirschman index (HHI)

is a commonly accepted measure of market concentration. It is

calculated by squaring the market share of each firm competing in a

market, and then summing the resulting numbers, and can range from close

to zero to 10,000.

Therefore, the Herfindahl-Hirschman Index is given by:

Part B:

Mane attraction, one of the firms with a 25% market share in the wig

manufacturing industry, leaves the market. This would cause the

herfindahl index for the industry to

increase.

The HHI increases as firms leaves the market. As firms leaves the market the shares of the market previously held by the leaving firms are shared amongst the remaining firms in the market thereby increasing the HHI.

For instance, assumint the firm with 50% of market share acquired additional 10% of the leaving firm's market share and the other firm with 25% acquired the remaining 15%.

The new HHI is given by:

</span><span><span>

</span>

Part C:

The largest possible value of the

herfindahl index is 10,000 because: an

index of 10,000 corresponds to a monopoly firm with 100% market share</span>.

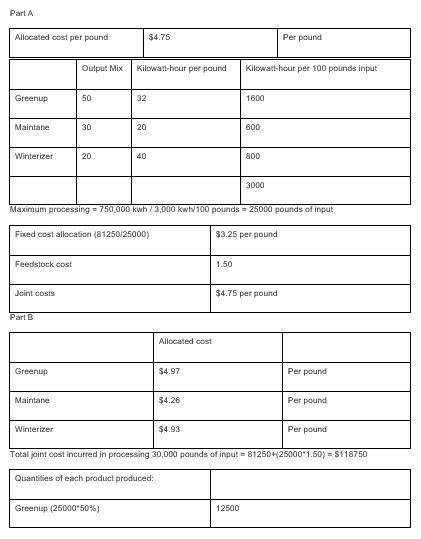

Answer:

See complete solution in the picture attachment.

Explanation: