Answer:

26.50%

Explanation:

Note: The full question is attached below

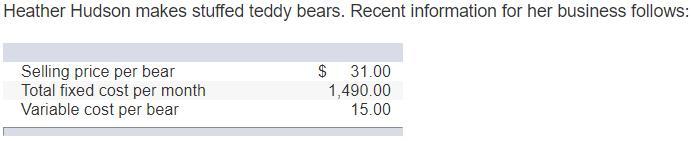

Contribution margin = Sales - Variable expenses

Contribution margin = $31 - $15

Contribution margin = $16

Current Proposed

Contribution margin $6,080 $7,296

<em> ($16*380) (6080*$1.2)</em>

Fixed Cost <u>($1,490</u>) <u>($1,490)</u>

Net operating income $4,590 $5,806

Increase in profit = ($5,806 - $4,590) / $4,590

Increase in profit = 0.2649237

Increase in profit = 26.50%