Answer:

a. Bonds payable Liability account

b. Equipment Asset account

c. Accounts payable Liability account

d. Salaries payable Liability account

e. Common stock Equity account

f. Retained earnings Equity account

g. Cash Asset account

h. Accounts receivable Asset account

i. Sales revenue Equity account

j. Inventory Asset account

Explanation:

All the assets account is debit in nature, so the equipment, cash, account receivable and Inventory accounts are debit in nature and these are classified as asset.

All the account with credit nature is either classified as Liability or Equity accounts. Equity accounts are common stock, retained earning and sales revenue. Liabilities accounts are bond payable, account payable and salaries payable.

Answer:

-$18,375

Explanation:

The computation of the net present value is shown below;

In the case when the operating cash flow is $56,200 for 5 years and the rate of return is 15.2% so the present value is $187,502 by using the financial calculator

In the case when the net after tax salvage value is $67,000 for the 5 year and the rate of return is 15.2% so the present value is $33,023 by using the financial calculator

Now the net present value is

= $18,7502 + $33,023 - $238,900

= -$18,375

Answer:

$8,693

Explanation:

Effective annual interets rate: AI = (1+i/m)^n - 1

i = 3*2=6%, m = 26

AI = [1+6%/26]^26 - 1

AI = 1.0617 - 1

AI = 0.0617

Let semi annual income be $X. So, present value of four semiannual income will be aggregated to get principal invetsed money of $30,000

30,000 = ∑[X/1.0617^n}

30,000 = 3.451 * X

X = 8693.132425383947

X = $8,693

Therefore, firm have to earn $8,693 after every 6 months at an interest rate of 3% per week to recover $30,000 initial investment in 2 years

Answer:

a. 1. You would want the regulatory boards to see more competition, so you would argue that the relevant market is all toys, which is as broad as possible. This would make it less likely that the merger would violate merger guidelines.

b. 2. You would want to use the narrowest definition of the market, which would be dolls. This would make it more likely that the merger would violate merger guidelines.

Explanation:

a. In order to avoid anti-trust laws, it would be best that Mattel convinces the authorities that the relevant category is all toys not just a subsection. This will show that the toys made by the new company would have a lot of competition from other toy makers across the board which would reduce their chances of being a monopoly and violate merger guidelines.

b. As the bid is unsolicited, Hasbro might want to defend against it. In which case their strategy should be the exact opposite of that of Mattel and they should try to convince the regulatory boards that they would be in the narrowest of markets which would be dolls. This would mean that the merger has a strong chance of leading to a monopoly and would violate merger guidelines.

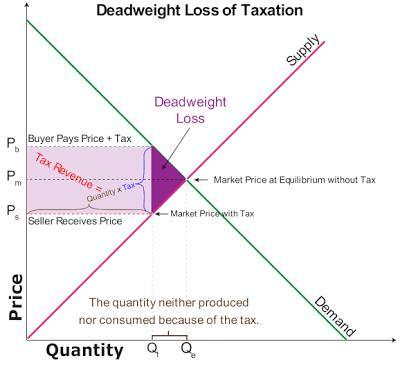

Answer:

A decrease in the size of a tax always decreases the deadweight loss of that tax.

Explanation:

Deadweight loss of tax is defined as the harm that is caused by tax to economic efficiency and prodction. It measures by how much taxes reduces the standard of living of a population.

Deadweight loss is the difference between to tax imposed and the reduction in production level it causes.

A decrease in the size of tax will give more income free to invest in production, therefore the production level will increase. This reduces the deadweight loss.

Effect of tax on deadweight is illustrated in the attached.