Answer: Financial disadvantage of -$863,000

Explanation:

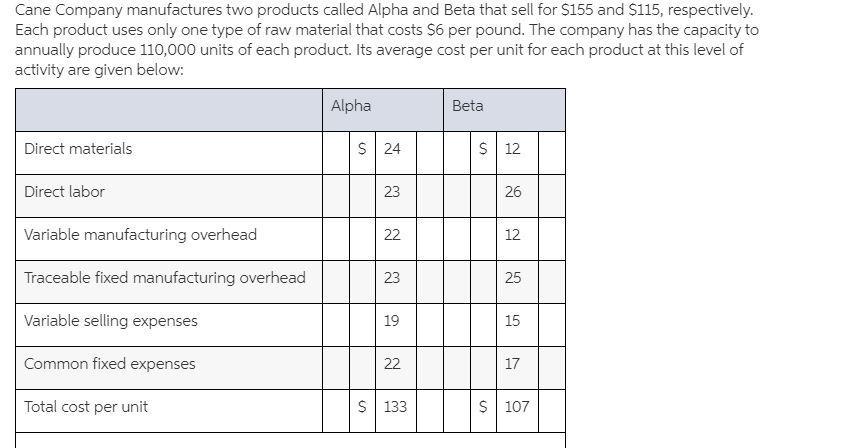

If they made the 87 thousand units themselves, they would incur a cost of:

= 87,000 * (Direct labor + Direct materials + Variable manufacturing overhead) + Traceable fixed manufacturing overhead

= 87,000 * (23 + 24 + 22) + (23 * 110,000)

= 87,000 * 69 + 2,530,000

= $8,533,000

<em>Traceable fixed costs are based on the total capacity of 110,000 units being produced and so will not change. </em>

If they buy from the supplier, the cost would be:

= 108 * 87,000

= $9,396,000

Financial advantage (disadvantage) = 8,533,000 - 9,396,000

= -$863,000