Answer:

E. Working harder.

Explanation:

Motivation is getting people to work in order to accomplish a set goal. It is also the process of bringing out the best in people by making them know the reason for motivating them, which is premised on their needs not yet fulfilled.

It is the duty of manager to influence his or surbodinate positively in terms of being productive in order to improve their capacity and efficiency. A well motivated employee will have on the job satisfaction and individual self development.

Employees can be motivated through payment of incentives like bonus for working extra hours or for working on weekend which is outside of the normal working days.There is also affiliation motivation, which is a desire to socially relate with people and achievement motivation, which is a desire to purse a goal and achieve it.

As in the case above, Randy might gnore his feeling of not being adequately rewarded and work harder in next quarter.

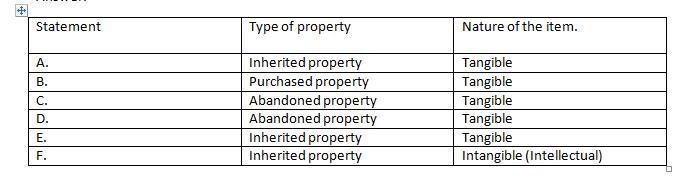

Answer:

I have formulated the answer in the table and the table is attached in the attachment please refer to the attachment 1.

Explanation:

<em>Please refer to the attachment 1. And here is the explanation</em>

Inherited property is the property which is transferred to ones beloved after she/he passes away or makes a will, so statement A, E and F are inherited properties.

Purchased property are the ones that one acquires after paying certain price of the good, so B is purchased property.

Abandoned property is the goods or intangible thing left somewhere and the owner is not known, so statement C and D are abandoned properties.

<em></em>

If a 10-pound bag of dog food sells for $6. 99, then $-3.01 is the per unit cost of the dog food.

The unit method is a method of solving a problem by first finding the value of a single unit, then multiplying the value of that single unit to find the necessary value.

For example, to solve this problem: How far does he walk in his 7 hours?", first calculate how far the person walks in his 1 hour. We can assume that he will run half the distance in half the time. Therefore, dividing by 2, the man said that in one hour he would walk 3.5 miles. Multiply by 7 by 7 hours and the man will walk 7 x 3.5 = 24.5 miles. That is, take the distance traveled by the man as X and divide by the given distance (7 (x/7)). equals the time it takes to travel X distance (7 hours) divided by the time it takes to travel 7 miles (2 hours) (7/2) so x/7=7/2 so X = 24.5 miles.

Learn more about Unitary Method here: brainly.com/question/19423643

#SPJ4

After missing<span> a </span>payment<span>, </span>you<span>'ll likely see two charges: A late fee, usually between $25 and $35, and interest on the balance. </span>If<span> the </span>missed payment<span> was an accident,</span>you<span> may want to call your issuer and explain that the </span>missed payment<span> was an accident, it won't </span>happen<span> again and </span>you<span>'ve already made a </span>payment<span>.

Have a wonderful day !!!!!! :) </span>

Allison Corporation acquired all of the outstanding voting stock of Mathias, Inc., on January 1, 2017, in exchange for $6,059,500 in cash. Allison intends to maintain Mathias as a wholly owned subsidiary. Both companies have December 31 fiscal year-ends. At the acquisition date, Mathias’s stockholders’ equity was $2,045,000 including retained earnings of $1,545,000