Answer:

Either because they are in high demand or are advertised well

Explanation:

Answer: Option B

Explanation: In simple words, perfect competition refers to a market structure in which there are large numbers of buyers and sellers each operating at a minor level in the market. Due to high number of participants and low level of operations no firm can individually affect the price.

In such a structure the prices are determined by the market forces of demand and supply.

Hence the correct option is B .

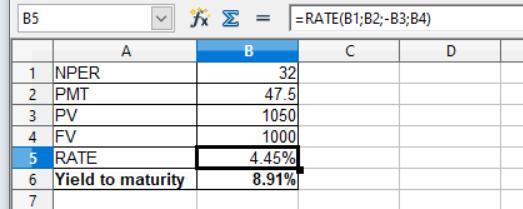

Answer:

8.91%

Explanation:

In this question We applied the Rate formula which is presented in the attachment below:

Data given in the question

PMT = 1,000 × 9.5% ÷ 2 = $47.50

NPER = 18 years - 2 years × 2 = 32 years

Present value = $1000 × 105% = $1,050

Assuming figure - Future value = $1,000

The formula is shown below:

= Rate(NPER;PMT;-PV;FV;type)

The present value come in negative

So, after solving this, the yield to maturity is 8.91%

Answer:

46.5%

Explanation:

The treasury bills have zero beta as they have no systematic risk. Beta is used in the Capital asset pricing Model to demonstrate a relationship between systematic risk and rate of return.

Expected Return = Rf + Beta * Rp

The percentage that should be invested in the risky portfolio will be,

1 - 1 / Beta

1 - 1 / 1.87

= 46.5%

Answer:

Medicaid can provide cost-sharing assistance. Depending on your income, you may qualify for the Qualified Medicare Beneficiary (QMB). If you are enrolled in QMB, you do not pay Medicare cost-sharing, which includes deductibles, coinsurances, and copays.

Explanation:

The Centers for Medicare & Medicaid Services (CMS) are responsible for implementing laws and various forms of guidance, sub-regulatory guidance operational updates and technical clarifications passed by Congress related to Medicaid and the Basic Health Program to explain what states and others need to do to comply.

There are 4 “metal” categories of health insurance plans: Bronze, Silver, Gold, and Platinum. These categories show how you and your plan share costs. Plan categories are independent from quality of care.

The total costs for health care include a monthly premium bill to the insurance company and out-of-pocket costs, which have a big impact on your total spending on health care and sometimes more than the premium itself as the out-of-pocket maximum is the amount you have to spend for covered services in a year, and only after you reach this amount, the insurance company pays 100% for covered services; and the deductible, which is the amount you have to spend for covered health services before your insurance company pays anything (except free preventive services). The Plan and network types allow you to use or not doctors or health care facilities. Plans & prices are issued according to the income and household information and they determine the copayments and coinsurance, which are payments you make each time you get a medical service after reaching your deductible

There are plans that have very low monthly premiums, but have high deductibles and pay less of your costs when you need care.

If you qualify for "cost-sharing reductions" (CSRs), Silver plans may offer good value because of a lower deductible. The income determines where your estimate falls in the range for cost-sharing reductions.

A Gold plan or Platinum plan generally have higher monthly premiums but pay more of your costs when you need many doctor visits or regular prescribed medication.