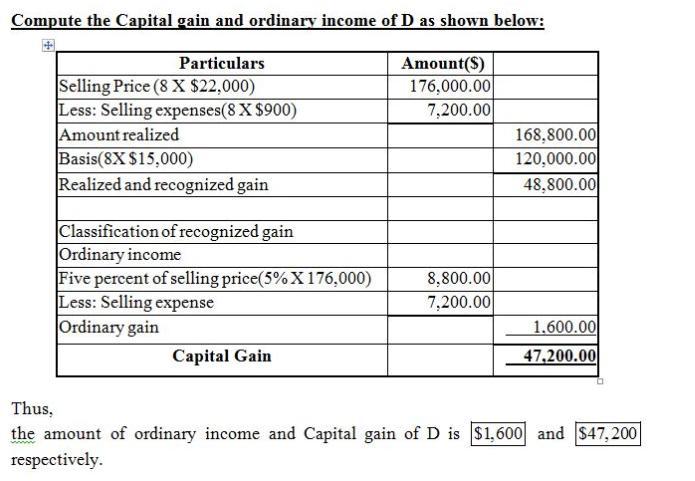

Answer:

Items a) and b)

a) items used currently in the production of goods to be sold items

b) held for resale items currently in production for future

Explanation:

Inventory consists of current assets to be used in production of final goods or are the ones which are final goods and held for sale.

In the given case also, statement a includes raw materials, which are used to make the final good to be sold, which is a part of inventory.

Further, statement b includes work in production or final goods which are currently in production but would be resold.

The items which are kept for their use as like machinery or furniture or which shall be disposed are not inventory but are in fixed assets category.

Answer:

the increase in additional paid in capital is $13,000

Explanation:

The computation of the increase in additional paid in capital is shown below:

= (Average price per share - par value of shares) × number of shares

= ($21 - $8) × 1,000

= $13 × 1,000

= $13,000

hence, the increase in additional paid in capital is $13,000

Answer:

Explanation:

Attached is a workbook with a schedule of Projected annual cashflow for Snow Inc.. The annual cashflow entries are projected using a rate of 8%. For instance, in the first year, our cashflows are not subject to any projection. But in the second year, the annual revenue of $1400000 is projected using the required rate of return.

Revenue (second year) = 1400000[1+0.08]^1

= 1400000 × 1.08

Revenue = $1,512,000

This technique was used to project the value for all cashflow elements for the rest of the years in consideration.