Answer:

$75,000

Explanation:

Revenue is said to be earned on the deliver of the goods and services to the party that enjoys the benefits from the good or service.

As long as control of the goods has been transferred, the revenue is earned. Note that this is not when cash has been collected.

As such, if the company earned $75,000 in 2018 but some amounts are to be collected in subsequent years, the revenue earned in 2018 is still $75,000 while the amounts yet to be collected will be recognized in accounts receivable.

Answer:

Saving can only be done in person. Investing can be done both in-person and online.

Explanation:

Saving refers to keeping some funds aside for use during emergencies. Individuals and institutions also save as a way of accumulating funds for a specific intention. Banks and other deposit-taking institutions offer saving services to pool funds and lend them for investment and consumption.

Saving will attract lower interest rates, sometimes below the inflation rate. Banks offer lower rates on saving and charges a higher interest rate to borrowers to make profits. Because saving offer lower returns, they are suitable for short-term periods. Savings are relatively safer than investment.

Investments offer higher returns but have a higher risk. Due to their price volatility, investments are suited for the long-term to safeguard against price fluctuations.

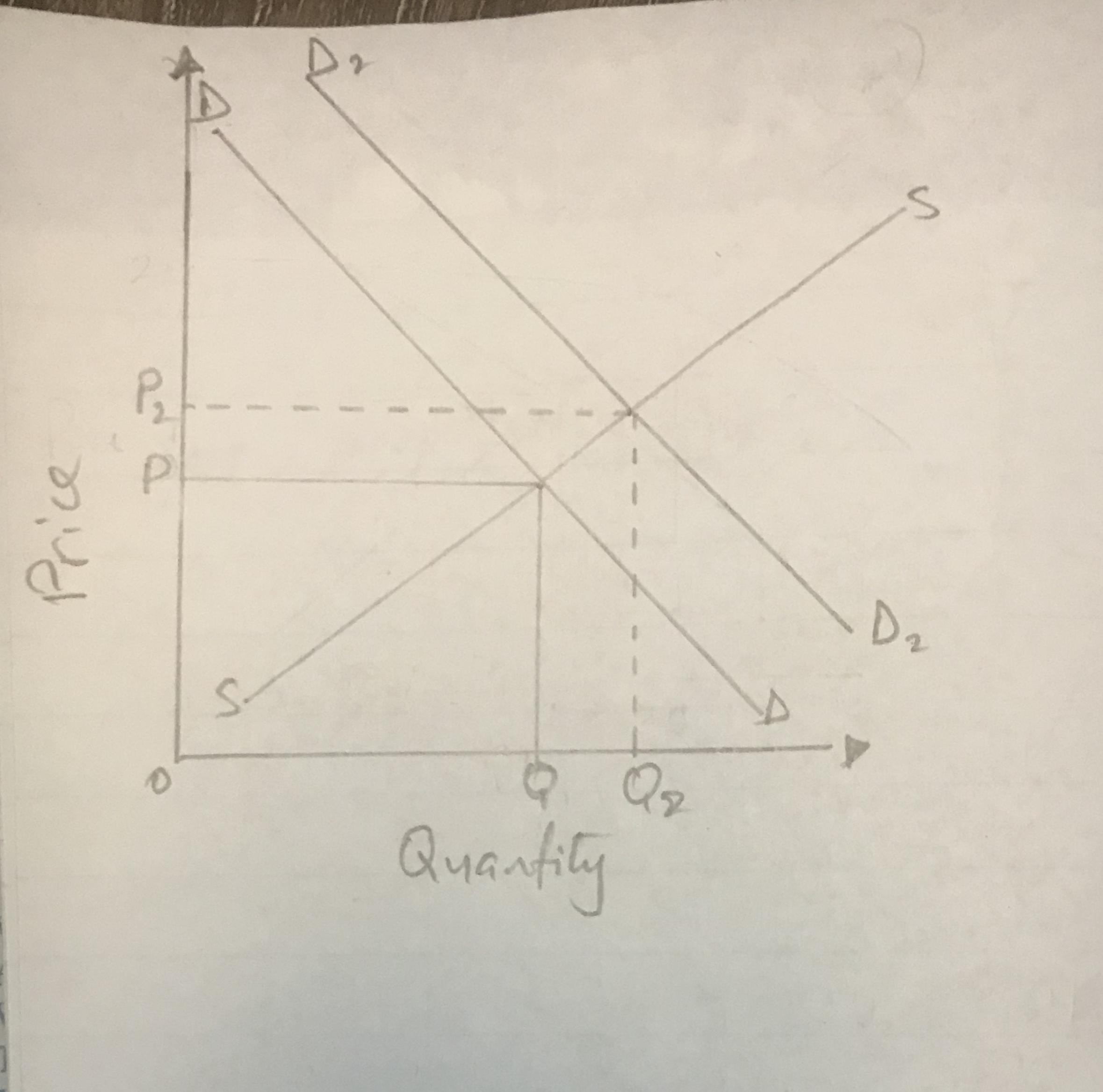

Answer: The correct answer is option B; Add D2 to the right of D, showing an increase in demand and increase in equilibrium price.

Explanation: The demand for a commodity is usually affected either positively or negatively by some factors or determinants. Foremost among the factors of demand is price of the commodity. Other factors include;

(a) Price of substitute commodities

(b) Consumers preferences

(c) Population

(d) Weather conditions

(e) Advertising

In the question above, the use of a popular actor as the spokesperson of the product is a form of advertising that is intended to improve upon the perception of the commodity and hence encourage consumers to buy more of it. If the popular personality endorses a product, there is an almost one hundred percent likelihood that consumers would see the product as a preferred choice and this would cause the demand to go up or increase.

An increase in the market demand would be signified by the outward shift of the demand curve to the right from D to D2. Since the x-axis shows the quantity demanded increasing towards the right hand side, then an increase in market demand would be reflected by a shift of the demand curve to the right.

As a result of that, the price would now move from P to P2 which shows an increase in equilibrium price. Also the quantity demanded would move from Q to Q2 which also indicates an increase in demand.

Solution :

In the context, the relevant tax issues are :

1. The transfer to be subjected to tax deferred treatment under 351. It is a tax issue for transaction.

2. Kathleen receives stock in the exchange of the property transferred.

3. Receipt of the stock that is a gift from her mother is a relevant tax issue.

4. If Kathleen is not the transferor of the property and Kathleen receives the stock from the corporation, the transaction will be qualify as non taxable under 351.

5. Stocks received by Kathleen and Nancy is a taxable and so it is relevant to the tax issue.

6. The property in the hands of a corporation is always a tax issue.

7. The deductions that is allowed when the transfer of the stock for the rendering services for Kathleen.

8. The transfer of the stock is considered as gift to Kathleen by Nancy is a taxable transaction, so it is a relevant tax issue.

Answer:

$1000

Explanation:

The cash received from the equipment sale is equals to the initial cost of the equipment which is $10,000 minus total accumulated depreciation on the equipment charged till date.

Total accumulated depreciation on the equipment=Opening balance of accumulated depreciation+depreciation charge for the year-closing balance of accumulated depreciation

Total accumulated depreciation on the equipment=$22,000+$4,000-$17,000

=$9,000

cash proceeds=$10,000-$9,000=$1000